Next-generation artificial intelligence (AI) data centers require a ton of energy, and one company that stands to benefit is Vistra (VST 1.25%). Vistra is an independent power producer that sells electricity on the open market and benefits from rising demand.

Since the start of 2024, Vistra stock has surged 324%, as investors pile into the stock amid surging electricity prices. However, after peaking around $220 per share, the stock has cooled a bit and is now 25% off its 52-week high. Here’s why the dip looks like a buying opportunity to me.

Today’s Change

(-1.25%) $-2.07

Current Price

$163.46

Key Data Points

Market Cap

$55B

Day’s Range

$162.26 – $168.49

52wk Range

$103.34 – $219.82

Volume

4.1M

Avg Vol

4.8M

Gross Margin

17.72%

Dividend Yield

0.55%

Vistra’s business model benefits from rising electricity demand

Vistra owns and operates multiple energy assets and is the largest competitive power generator in the United States. The company has 44,000 megawatts (MW) of total capacity, including 24,000 MW of natural gas and 6,400 MW of nuclear, making it the second-largest nuclear operator in the U.S., behind Constellation Energy.

Image source: Getty Images.

It operates as an independent power producer (IPP), also known as a merchant power company, and sells its energy into competitive markets, meaning it takes prevailing market prices for its electricity. This contrasts with regulated utility providers, such as Duke Energy, which operate in specific regions and have rates set by regulators. Regulated utility providers also own the entire energy chain, from power plants to transmission lines.

Rising electricity demand from data centers has been a boon for Vistra and other IPPs, as their business models enable them to capture the upside of higher electricity prices. Because data centers require low-carbon, reliable baseload power, many have turned to Vistra thanks to its massive nuclear footprint. This year, the company has entered into 20-year power purchase agreements (PPAs) with companies such as Amazon and Meta Platforms.

Regulations could impact its profit potential

However, the company isn’t shielded from regulations that impact its business. For example, if regulators impose price caps on electricity, wholesale sellers like Vistra will lose the ability to capture the upside.

In the PJM Interconnection region of 13 states and Washington, D.C., which spans the Midwest and Mid-Atlantic, the 13 governors have sought to extend price collars for the 2028/2029 and 2029/2030 auctions, which would limit how high capacity prices can rise.

On top of that, regulators at the Federal Energy Regulatory Commission (FERC) could begin to scrutinize colocation deals between Vistra and hyperscalers if those deals shift costs onto residential customers. These pressures are what have weighed on the stock in early 2026.

Vistra trades at a more attractive valuation today

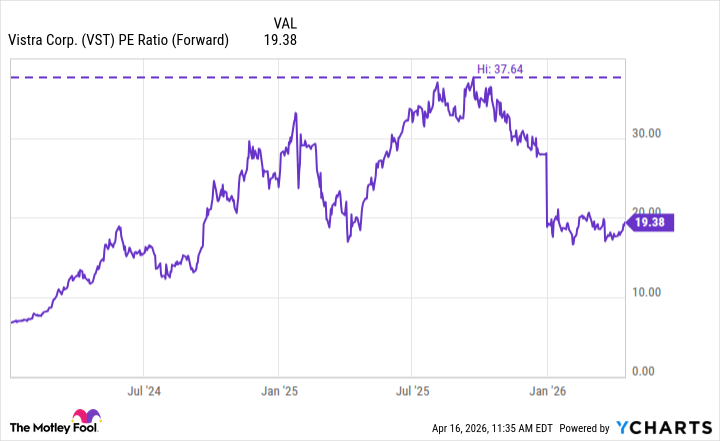

Vistra faces uncertainty as regulators grapple with rising electricity demand and prices and seek to protect consumers from them. As a result of its 25% decline, the stock has de-risked to some degree and is now priced at 19.3 times forward earnings, down from its peak of 37.6 times last fall.

Data by YCharts.

That said, Vistra will benefit from growing demand and continue adding to its energy capacity to meet it. It recently announced plans to acquire Cogentrix Energy for $4 billion, which adds five,500 megawatts (MW) of natural gas capacity in the PJM and ISO-NE regions, where data center power demand is surging. Given its portfolio of energy assets in key U.S. regions, I think now is the time for investors to buy the dip in Vistra stock.