Stock investors have been hearing about artificial intelligence (AI) chips for multiple years and watched as chip company Nvidia (NVDA +1.67%) became the world’s most valuable publicly traded company. Concerns about an AI bubble seem to be fading as chipmakers continue to post strong fundamentals that have correlated with meaningful stock gains.

Grandview Research projects a 29% compound annual growth rate (CAGR) for the AI chip industry from 2024 to 2030, which suggests AI chip stocks still have upside.

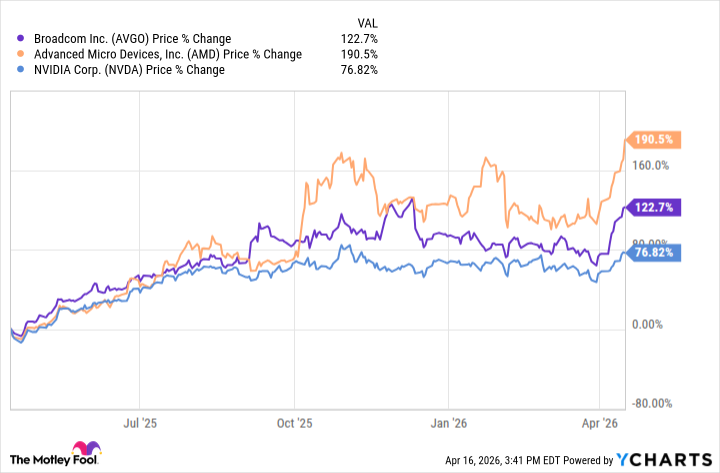

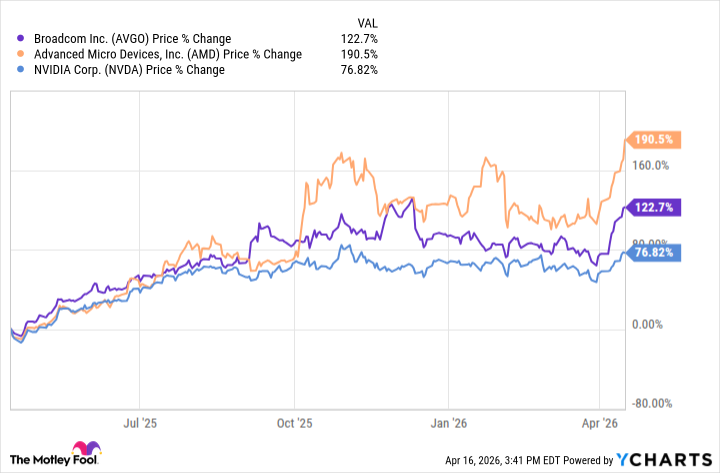

While all eyes are on Nvidia, there are other AI chipmakers that can produce higher returns. Broadcom (AVGO +2.02%) and Advanced Micro Devices (AMD +0.05%) have both outpaced Nvidia year to date and over the past year. Broadcom specializes in custom AI chips that vary for each customer, while AMD functions more like Nvidia, offering GPUs (graphics processing units) that can handle a wide range of workloads.

While Broadcom and AMD investors have both had plenty of things to be happy about recently, a head-to-head match-up gives investors a lot to consider.

Image source: Getty Images.

Both companies have grown partnerships with big tech

Broadcom and AMD sell AI chips to the top companies in the tech industry. Those customers have deep pockets, which have helped both AI chipmakers deliver exceptional revenue growth. Some of those long-term partnerships got even deeper recently.

Today’s Change

(2.02%) $8.04

Current Price

$406.51

Key Data Points

Market Cap

$1.9T

Day’s Range

$399.81 – $406.73

52wk Range

$161.61 – $414.61

Volume

618K

Avg Vol

26M

Gross Margin

64.96%

Dividend Yield

0.61%

AMD and Meta Platforms (META +1.81%) recently partnered to deploy 6 gigawatts of AMD GPUs, with shipments supporting the first gigawatt deployment set to start in the second half of the year. AMD CFO Jean Hu told investors to expect “substantial multiyear revenue growth” due to the partnership.

Broadcom also announced an extended partnership with Meta Platforms to supply custom-made AI chips for multiple gigawatts.

Broadcom also recently expanded its partnership with Alphabet (GOOG +2.00%) (GOOGL +1.71%) and Anthropic. The latter is investing in additional Google Tensor Processing Units (TPUs), and Broadcom produces TPUs. It’s another testament to how much momentum custom-made AI chips have gained in recent years.

AMD is currently growing faster

Broadcom has enjoyed better headlines than AMD this year due to its expanded partnerships with Meta Platforms, Alphabet, and Anthropic, but both companies have exceptional customer rosters. They have top-tier semiconductors that fulfill their roles and have become high-demand products enjoying multiyear tailwinds.

Today’s Change

(0.05%) $0.13

Current Price

$278.39

Key Data Points

Market Cap

$454B

Day’s Range

$274.14 – $281.05

52wk Range

$83.75 – $281.05

Volume

36M

Avg Vol

38M

Gross Margin

45.99%

Both companies have also delivered exceptional financial growth, but a closer look at those numbers starts to hint at which company may present the better buying opportunity. Broadcom delivered 28% year-over-year revenue growth in the fourth quarter of fiscal year 2025, ended Nov. 2, compared to AMD’s 34% year-over-year revenue growth during roughly the same stretch (AMD’s fiscal year ended Dec. 27).

Those numbers are close, and they actually get a bit narrower when analyzing long-term trends. They have nearly identical 10-year revenue compound annual growth rates (CAGRs), with Broadcom posting a 27% CAGR compared to AMD’s 26.8% CAGR. AMD has a higher five-year CAGR, while Broadcom has a higher three-year CAGR.

AMD’s guidance implies 32% year-over-year revenue growth at the midpoint for its current quarter. The company is expected to report in early May. Broadcom reported earnings results for its fiscal first quarter of 2026, which ended on Feb. 1, in early March. Those results showcased 29% year-over-year revenue growth. That’s solid, but it’s a little less than what AMD expects.

Margins could be the fuel

Both of these growth stocks are leaders in a high-growth industry with the right partnerships. They are excellent businesses with high revenue growth, but AMD looks to be boosting sales slightly faster than Broadcom.

The decisive factor for investors might be how much they believe in AMD’s ability to expand margins. Although AMD wins on revenue growth, Broadcom crushes AMD when it comes to profit margins. Broadcom had a 47.3% net profit margin in Q4 2025 and a 38.1% net profit margin in Q1 2026. While profit margins can fluctuate, Broadcom is clearly doing an excellent job of retaining revenue. AMD registered only a 14.7% net profit margin in Q4, aftera 13.4% net profit margin in Q3.

While Broadcom has superior margins now, AMD has more room for improvement. If AMD gets its profit margin closer to Broadcom’s, the company could realistically triple its profits even if revenue stays stagnant, which seems extremely unlikely.

Less than a year ago, AMD had net profit margins in the mid-to-high single digits, so there is a recent history of rising margins. Broadcom is the better business right now, but investors who believe AMD can improve its profit margin quickly may want to buy its stock instead.