The market is crowding into any stock deemed a winner of the artificial intelligence (AI) revolution. All other stocks are seeing liquidity drained from their share prices if they are unassociated with AI, such as Nu Holdings (NU +0.73%), even though the Latin American digital banking giant is growing like gangbusters and has seen a profit inflection.

Shares of Nu Bank are down about 30% from recent highs. Here are three reasons the stock looks like a screaming bargain for investors right now.

Today’s Change

(0.73%) $0.10

Current Price

$13.14

Key Data Points

Market Cap

$64B

Day’s Range

$13.01 – $13.24

52wk Range

$11.71 – $18.98

Volume

1.4M

Avg Vol

51M

More Latin American growth

The core of Nu’s business today is in Brazil, its home market, and Mexico. It operates in Colombia, but that is an inconsequential market for revenue today.

Brazil and Mexico are at two different maturity stages but still have great growth prospects during the next few years. Nu Bank has almost 100 million active customers in Brazil out of a population of 213 million, meaning growth is not going to come from new user acquisition. It is adding new products across its digital banking ecosystem to generate more revenue from each customer. You can see this in the consolidated monthly average revenue per customer, which hit $16 last quarter, up from $3 at the end of 2020.

But in Mexico, Nu Bank still has a long runway to expand its banking service. It has 15 million customers, growing from a standing start a few years ago, compared to Mexico’s population of 133 million. It wouldn’t be shocking if half the population of Mexico were using a Nu Bank product in one form or another in five to 10 years.

Image source: Getty Images.

A controversial expansion into the U.S.

Outside of Brazil, Mexico, and Colombia, Nu’s next target is actually the U.S. This was a controversial decision for the bank, as the U.S. is a highly competitive market with the world’s biggest banks and many digital disruptors in the same mold as Nu Bank.

Management believes it has an angle worth pursuing in the U.S., though it hasn’t yet laid out any specifics. My guess is that it will target lower-income customers, as it has in Brazil and Mexico, with better lending models, and will also focus on the country’s growing Latino population. At the same time, Nu will allocate only a small portion of its annual operating budget to the U.S. once it enters the market, which won’t weight on its profitability.

If it fails, investors will only see a small, expensive headwind for a few years. But if Nu Bank can expand to millions of customers in the U. S., it has a chance to build a business the same size as its Brazilian segment within the next decade. That is why the company is targeting the country as its fourth market, given its vast economy.

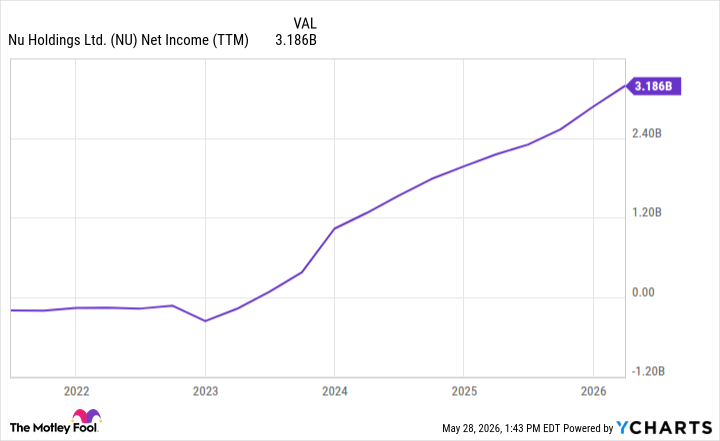

NU Net Income (TTM) data by YCharts.

Underrated efficiency gains

What Nu Bank is also underrated for is its ability to operate efficiently at a larger scale. Net income has exploded, up 4,000% during the past five years from close to breakeven to $3.2 billion.

This still underrates the true profit potential for the digital bank. It is spending heavily to market to customers in Mexico and Colombia while spending money to obtain its banking charter in the U.S. Net income grew 41% year over year last quarter, compared to 27% gross profit growth. Expect more of the same in the years ahead, as a similar level of overhead costs is spread around the expanding business.

Right now, Nu Bank has a market cap of about $64 billion. Earnings should keep tracking higher, approaching its current 41% growth rate during the next five years. This could help net income grow from $3.2 billion today to $10 billion in a shorter time than investors think, making the stock a bargain at these prices.