")

Stock Instead")

I want to think that my portfolio is fairly balanced. I own tech stocks that put me in a position to benefit from the sector’s high growth, and I also own dividend-paying stocks that return value regardless of day-to-day stock price performance.

High-growth tech stocks get much of the attention, but dividend stocks contribute meaningfully to many investors’ portfolios. It’s an under-the-radar gift that keeps giving in many cases. Not all dividend stocks are created equal, but two that I own and will keep for the long haul are Coca-Cola (KO +0.38%) and Walmart (WMT 0.82%).

I wouldn’t hesitate to double up on them right now because I know I can treat them as set-it-and-forget-it stocks.

Image source: The Motley Fool.

The beverage king continues to reign supreme

Coca-Cola is one of the legacy blue chip dividend stocks on the market. It has worldwide brand recognition, timeless products, and an unmatched distribution network. It’s a trifecta you want from any stock but especially a dividend stock.

One of the smartest moves Coca-Cola made was going to an asset-light business model. Although you can walk into your local convenience store or restaurant and buy a Coca-Cola product, the company doesn’t actually bottle or can the finished product. Instead, it sells concentrates and syrups to its distribution partners, which then handle bottling and distribution.

Not only has this helped Coca-Cola expand its distribution by relying on local distributors more familiar with the landscape and logistics, but it has also improved margins because it doesn’t need as many trucks or other costly machinery.

Today’s Change

(0.38%) $0.31

Current Price

$81.48

Key Data Points

Market Cap

$351B

Day’s Range

$80.92 – $81.67

52wk Range

$65.35 – $82.66

Volume

8.2M

Avg Vol

15.3M

Gross Margin

61.82%

Dividend Yield

2.53%

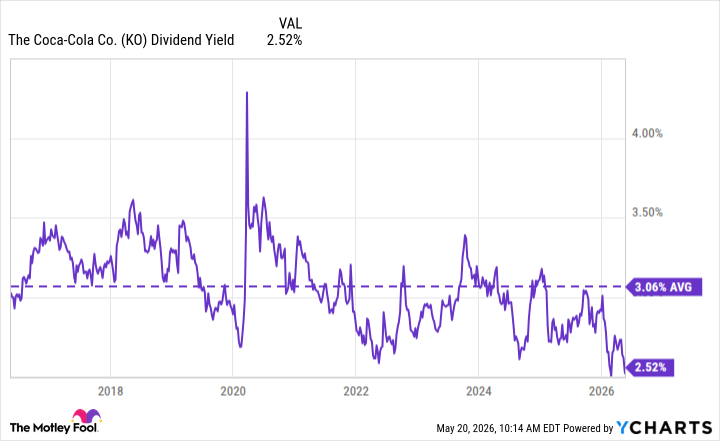

Coca-Cola is a company whose dividend you don’t have to second guess. It’s a Dividend King (a company with at least 50 consecutive years of dividend increases), with 64 consecutive years under its belt. The company knows that growth is limited at its current size, so the main draw for investors is the dividend. It prioritizes its dividend and has the financials to do so comfortably.

In its most recent quarter (ended April 3), Coca-Cola reported net income of $3.92 billion and paid $2.28 billion in dividends ($0.53 per share). That 58% payout ratio is in line with the healthy range that investors should want to see.

I don’t own Coca-Cola stock expecting double-digit annual growth; I own it for its reliability. Its products sell no matter the state of the economy, and its dividend has consistently been attractive. Over the past decade, it has averaged a 3% dividend yield, far more than the S&P 500 average over that span.

KO Dividend Yield data by YCharts.

The evolving retail giant you can’t miss

Walmart also sits firmly in the group whose products sell regardless of broader economic conditions. Going through rough times and looking for value? Walmart’s got you. Financially comfortable with not many cares? You still can’t beat the convenience of Walmart.

Up until this past year, Walmart brought in more revenue than any other public company in the world. With so much volume, it can prioritize keeping prices low, and that’s a business angle that’ll never go out of style. People will always appreciate low prices.

Today’s Change

(-0.82%) $-0.99

Current Price

$120.35

Key Data Points

Market Cap

$959B

Day’s Range

$118.91 – $121.92

52wk Range

$93.43 – $135.16

Volume

1.5M

Avg Vol

19.3M

Gross Margin

23.48%

Dividend Yield

0.80%

Walmart isn’t a traditional dividend stock with an above-average yield. Its current yield is just above 0.7%, with an average of 1.7% over the past decade. On one hand, the low yield is due to Walmart’s stock having experienced significant growth over the past few years (up 178% in the past five years, as of May 20). On the other hand, much of the appeal is the consistency. Walmart is also a Dividend King, with 53 consecutive dividend increases.

You never have to question Walmart’s finances — it made $713.2 billion in revenue and $22.3 billion in net income in its last fiscal year — and its business is improving in areas that almost guarantee the company becomes more profitable.

Memberships, advertising, and the marketplace are three key high-margin business areas in which Walmart is showing impressive growth. They’re much higher-margin businesses than retail, so I expect to see continuous bottom-line improvements. You can bet the dividend will only get stronger over time.