Author’s note: This essay assumes that readers have a basic familiarity with options — like the difference between puts and calls, and the difference between buying and selling options. If you don’t, our options trading glossary may come in handy. The investment positions, opinions and predictions described here are mine alone and should not be interpreted as financial advice, nor are they attributable to NerdWallet as a whole.

My 5 options selling lessons 💡

I like to think I’m a pretty smart guy. I have an economics degree, I’ve been writing about investing for most of my adult life, and I’m generally pretty clever and thrifty with money. So I must know what I’m doing in the markets. Right?

That’s why I made the decision so many overconfident investors have made before me: To trade options. But I wasn’t going to buy puts or calls. Oh no.

I had a fancier plan: I was going to enter and exit positions by selling options on them, earning premiums and capital gains in the process. I am definitely the first person in the centurieslong history of financial markets to think of this idea.

Well, at the time of writing, I am still on my option-selling journey, and I’m pleased to report that it’s going… okay. It hasn’t been a disaster, but it also hasn’t been the easy money I’d hoped for.

Below, I’m sharing some lessons I’ve learned from the world of options selling. But first, allow me to introduce my strategy in more detail…

Make sense of the markets with The Nerdy Investor

Market news, economic forecasts and investing terms that actually matter to you (plus the latest in broker tech).

The plan: Buy an emerging markets ETF by selling puts on it. Then sell calls on it for a higher price.

I figured that this option-selling experiment would work well with a value investing strategy — enter an investment (by selling puts) that has experienced a drop in price recently, hold it for a while, and then exit it (by selling calls) after it has recovered.

Many of history’s greatest investors, like Warren Buffett, have made their fortunes through value investing, but it does have risks. Individual companies don’t always recover from a downturn; sometimes they go bankrupt. Industries, too, can become obsolete. Even countries can default on their sovereign debt or suffer geopolitical misfortunes that lead to years of economic malaise.

But what about an entire continent? My thought is, Africa can’t go out of business. Its financial markets might experience periods of volatility. But ultimately, it’s full of fast-growing emerging markets (like Egypt and South Africa) and frontier markets (like Kenya and Morocco), and is the youngest continent in terms of population (the median age in Africa is about 20.)

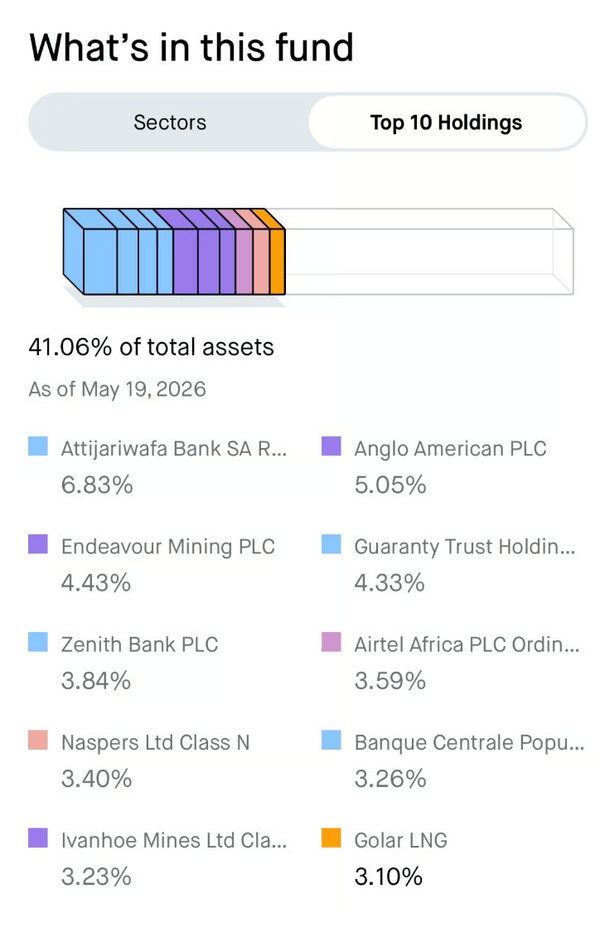

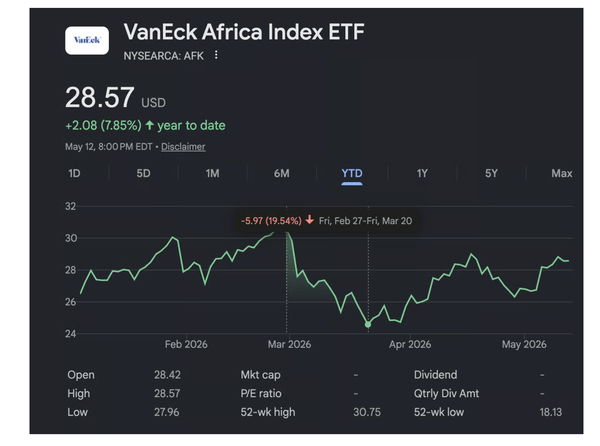

I think Africa is primed for long-term economic growth, so I wanted to try out my option-selling/value-investing experiment on an ETF of African companies. And it turns out there’s an ETF out there that gives you exposure to some of the largest publicly-traded companies on that continent: The VanEck Africa Index ETF (AFK).

I started eyeing AFK in late January of this year, when its price was bouncing between $28 and $30, and I bought into it in late February. Here’s what I’ve learned so far.

Five things I learned by trying to be an option-selling shark:

1. Options premiums can juice your returns. Sometimes. Very slightly.

When you enter a stock or ETF by selling a put option on it that gets exercised, the premium per share you earn from the sale gets subtracted from your cost basis on the stock or ETF. And when you exit a position by selling a covered call that gets exercised, the premium per share you earn gets added to your sale price. Many brokers, including Robinhood, which I’m using for this experiment, do these calculations for you automatically.

I figured that these premiums could really turbocharge my returns by lowering my cost basis and increasing my sale proceeds. And my theory is working well so far, if you allow for a very generous definition of the word “turbocharge.”

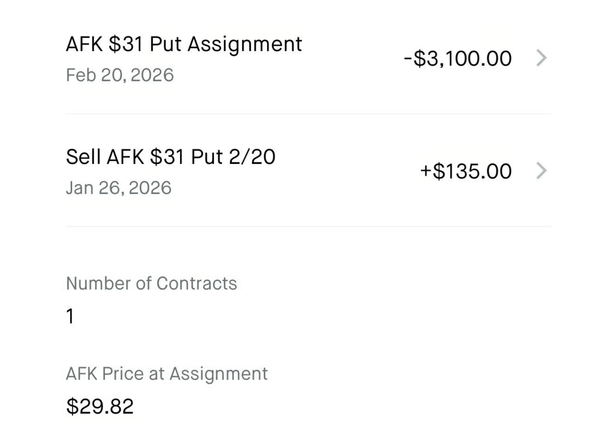

I bought my first 100 shares of AFK earlier this year by selling a put contract with a strike price of $31 for a price of $1.35 per share, or $135 in total. On Feb. 20, the option’s expiration date, AFK closed at $29.82, which was below my strike price of $31 — so my put option was exercised, obligating me to buy 100 shares of AFK for $31 per share, or $3,100 total.

But after subtracting the $1.35-per-share premium I earned, my net cost per share was just $29.65 — a discount of 17 cents per share from the market price of $29.82, or $17 on the entire contract. Turbocharged returns indeed.

The point is that if you enter an investment by selling a put option on it, then that means that the market price of the underlying investment at expiration was some amount below the strike price. As a result, your discount will be some amount less than the premium you earned.

2. You can profit by “selling high and buying low.” But will you?

One way options sellers can make quick money (in theory) is by selling an option for a high price, and then closing out the trade by buying that same option back at a lower price. It’s kind of like you’re short selling an option contract.

For example, you can profit if you sell a covered call when the underlying stock or ETF is climbing toward the strike price, and then buy the call back for cheaper if the underlying turns downward and falls away from the strike price.

But this strategy is risky. You might sell a sell a call on a stock or ETF that just keeps climbing until expiration. If the market price of the underlying crosses your option’s strike price, your option will likely be exercised, and you won’t get the chance to buy it back for a lower price.

And if you’re prone to nerves, you also run the risk of selling low and buying high.

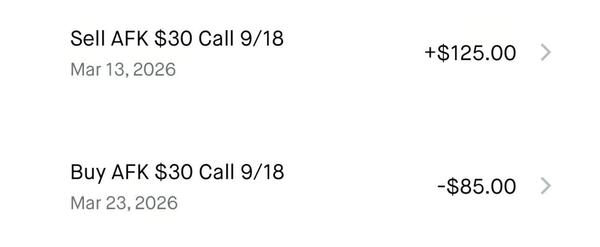

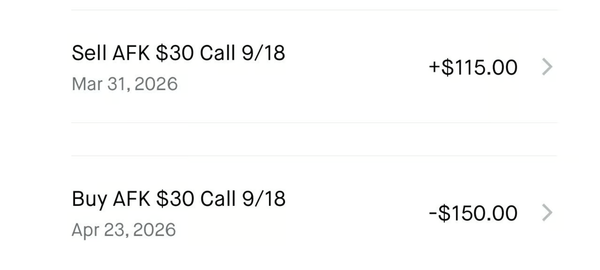

I once made a little profit of $40 by selling a covered call contract on AFK for $125 (when the ETF was climbing, before the Iran war broke out) and then buying it back for $85 (after the war broke out and emerging market ETFs like AFK went into a tailspin).

A week later, I tried to do the same thing again, but messed it up by being skittish, and promptly nerfed most of that profit. I sold a covered call on AFK for $115, and then got freaked out because the stock kept climbing, and then bought it back for a much higher price of $150, realizing a $35 loss on the contract.

(And, just my luck, AFK gapped downward a few days later, which would have given me the opportunity for another quick “sell high, buy low” profit. Oh well.)

3. You can’t earn much by selling options that are way out of the money.

When it comes to some stocks and ETFs — particularly those with low options trading volume, like, say, AFK — options traders are not particularly interested in buying puts with strike prices way below market price, or calls with strike prices way above market price.

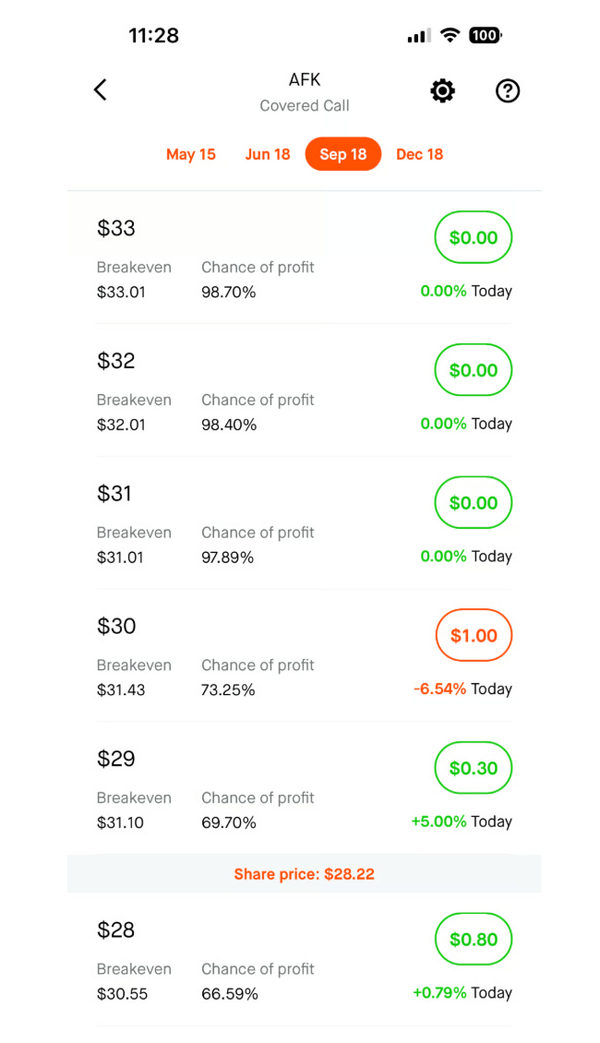

Here’s a screenshot of some out-of-the-money call options with an expiration date of Sep. 18 on AFK, which traded for $28.22 at the time of this screenshot.

If you’re looking to earn $1 or more per share ($100 or more per contract), you’ll generally need to sell options that are at substantial risk of getting exercised (that is, options whose strike prices are close to the underlying stock or ETF’s market price).

4. Liquidity matters. You don’t want to be the only person in the market.

I was actually correct in my belief that almost no one else has thought of trading options on emerging markets ETFs. But it turns out that that’s not entirely a good thing.

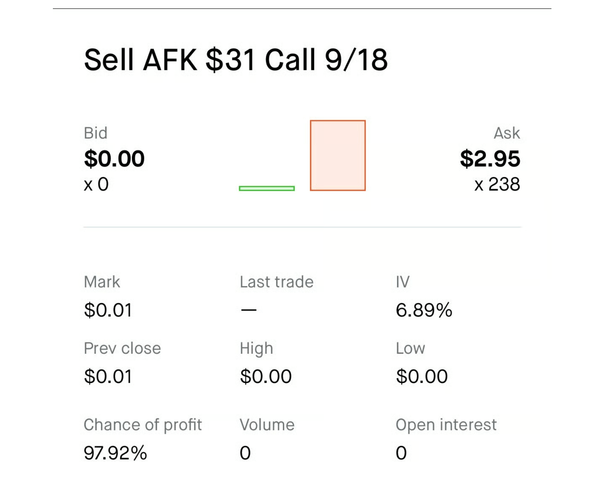

The market for options on the AFK ETF is an illiquid market, meaning that there’s a scarcity of buyers and sellers. Below is a screenshot of an AFK call with a strike price of $31 and an expiration date of Sep. 18 that I’ve tried to sell a few times.

I would have happily accepted a price below $2.95 per share on these attempts, but there are four numbers in the screenshot above that have foiled these attempts: Zero bids, no last trade, zero volume and zero open interest. Simply put, there is no one on the buy-side of the market for this call, which means that no transactions have taken place, and none can take place.

A lack of liquidity can also exacerbate the problem described in lesson #2.

If you were trying to “short-sell” an option contract — as in lesson #2 — then the lack of buyers and sellers for an option like the one shown above would make it hard to make the initial sale. And even if someone did wander into this part of the AFK options market and buy your call, the lack of liquidity could make it very difficult to buy your call back for cheaper, if you were trying to avoid getting exercised.

5. Option-selling profits are predictable. They just might not be high.

To review: I bought 100 shares of AFK by selling a put contract with a strike price of $31 for $1.35 per share, which was exercised on its expiration date of Feb. 20, giving me a net cost basis of $29.65 per share on that contract, or an initial investment of $2,965.

And I recently sold a covered call contract with a strike price of $32 for $1.10 per share. If it is exercised upon its expiration date of Dec. 18, it will bring in net proceeds of $33.10 per share on that same contract, a total of $3,310, netting me $345 in profits.

This would work out to a profit margin of 11.64% over a period of slightly less than 10 months, or about 14% on an annualized basis.

This wouldn’t be a bad result. It would be more than the S&P 500’s long-term average annual return of 10% per year. (Maybe I’m smart after all.)

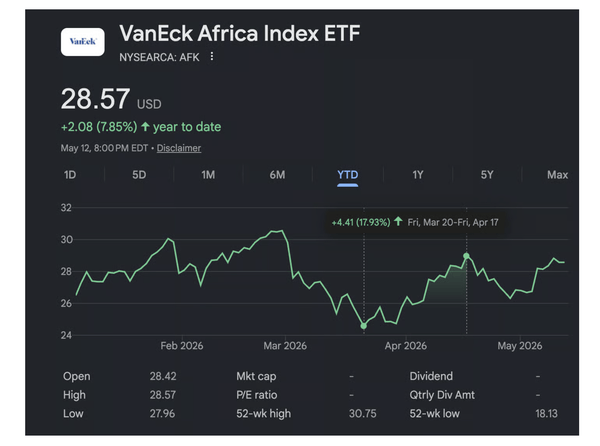

Except… I would be taking about 10 months to make an 11.64% profit. Hypothetically, a trader could have made way more than that within a single month if they’d bought the AFK ETF outright at its March low and then sold it at its April high.

Of course, that would have been a very lucky trader. It’s worth remembering that we can only definitively identify those relative highs and lows in hindsight.

I could have done much worse by trading without selling options.

It’s true that a lucky ETF trader could have earned a 17.93% profit on AFK by buying it in mid-late March and selling it in mid-late April.

But it’s also true that an unlucky ETF trader could have lost 19.54% on AFK in a matter of weeks, by buying it in late February and selling it in mid-late March.

As you may recall, I actually did buy into AFK in the second half of February. But I wasn’t so unlucky to buy it at its highest price for 2026, and — thanks to my put option premium being subtracted from my cost basis — I bought it at a de facto discount from its market price.

In a sense, my commitment to exit my AFK position by selling covered calls has saved me from panic-selling for a massive short-term loss like the hypothetical unlucky trader above.

When I’ve sold covered calls, I’ve always sold them at a strike price and premium which would be greater in sum than my cost basis, ensuring that I’d earn a profit if they were exercised. And if they weren’t exercised, then I’d get to keep the premium and try to covered call-sell out of my position again another day.

In conclusion: I don’t know if I’m smart enough to make good money selling options. But I’m definitely not smart enough to make good money trading the underlying investments outright.

If my options-selling misadventures sound like fun to you, and you have enough money to do this kind of medium-high risk speculation without jeopardizing your overall financial position, then you’d probably benefit from finding a good options broker. NerdWallet’s roundup of the best options trading platforms is a great place to shop around.

But also, if this sounds like fun to you, you might need better hobbies. Maybe I do too.

Disclosure: The author held shares of AFK at the time of publication.