Top investors like Warren Buffett consistently say their favorite stocks are ones they can hold forever. If you have a high-quality business compounding value, it is highly favorable for you and your retirement account to sit back and let the wealth pile up. $10,000 invested in a stock yielding a 20% annual return will grow to just $25,000 after five years. But if you hold that same stock for 20 years, it will be worth $383,000. That could be much more meaningful to your retirement savings.

With this in mind, here are three high-quality disruptors I believe are great holds for the next 20 years, and why investors should consider buying today.

Image source: Getty Images.

1. A storied entertainment brand

The most important factor in finding a stock to hold for 20 years is business durability. Perhaps no brand has been more durable in entertainment over the last few decades than Nintendo (NTDOY 1.39%). The family-friendly giant focused on gaming continues to develop high-quality content and remains the leading video game console seller worldwide.

It recently launched the Nintendo Switch 2 as its new flagship gaming hardware for the next five to 10 years, and it is selling like hotcakes. Twenty million units were sold last fiscal year ending in March, with close to the same projected in its second year at retail.

Today’s Change

(-1.39%) $-0.16

Current Price

$11.38

Key Data Points

Market Cap

$52B

Day’s Range

$11.33 – $11.47

52wk Range

$10.39 – $24.92

Volume

2.2M

Avg Vol

3.2M

Gross Margin

39.17%

Dividend Yield

0.59%

Nintendo’s business model works by selling gaming hardware to players at a thin profit margin, then making up the difference through high-margin game sales from first-party brands like Mario, Zelda, and Pokémon. The same playbook is being followed with the Nintendo Switch 2. Mario Kart World has sold 15 million copies, while a new Pokémon game sold 2.2 million copies within just four days after launch.

I expect the same playbook to work 20 years from now. With the stock down 54% from its highs amid fears over memory chips, Nintendo looks like a stock experiencing short-term pain that will deliver long-term gains for any investor who buys now.

2. The disruptor taking over the health insurance market

No industry is perhaps more durable than healthcare. Everyone around the world needs some level of healthcare coverage, making the health insurance market a staple of the United States economy. Even if customers dislike their health insurance provider, they still have to pay premiums each and every year.

Oscar Health (OSCR +2.26%) is a new health insurance provider that aims to delight customers. Instead of bogging down users in confusing paperwork and unclear expenses, Oscar has built a cloud-based health insurance platform from the ground up that is much easier for all stakeholders to use.

With this technology advantage, Oscar Health has attacked legacy players in the individual payor market from the Affordable Care Act marketplace. Through consistent nationwide expansion of its coverage, the business has gained more and more individual health insurance customers each year. Last quarter, it hit 3.2 million paying customers, up from 1 million in Q1 2022.

These customer gains are helping Oscar Health scale up and finally turn a profit. This year, it is guiding for $19 billion in revenue and $250 million to $450 million in operating earnings. Compared to its current market cap of $6.8 billion, the stock looks mighty cheap if you believe it can keep stealing market share in health insurance in the coming years.

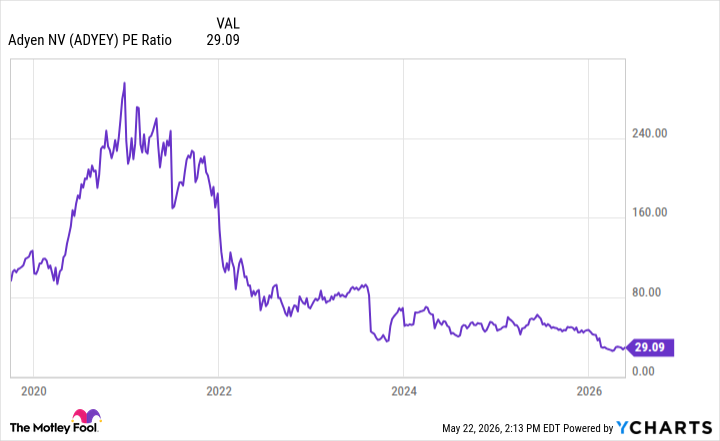

ADYEY PE Ratio data by YCharts

3. An underrated presence in payments processing

No matter how the economy evolves, retailers will need to process payments from customers worldwide, both offline and online. Adyen (ADYEY +0.92%) believes it has the best payments infrastructure for global corporations, which is why it is gaining market share in payments processing.

It touts customers such as Spotify and Uber with complex processing needs, where Adyen can deliver the best execution — meaning the highest percentage of payments that actually succeed at checkout — compared to the competition.

The financial results show this outperformance and market share gains. In Q1 2026, Adyen’s processed volume grew 21% year over year, with revenue growing 20% in constant currency. From 2016 through 2025, its revenue has grown by more than 10-fold as more enterprises adopt its checkout terminal for retail payments.

Right now, Adyen’s stock is down in the gutter, off 66% from all-time highs, with a price-to-earnings ratio (P/E) of 29. With plenty of room to keep growing market share and a durable addressable market in retail payments, Adyen looks like a great opportunity for investors right now.