Insurance costs have risen in recent years, and the rate hikes are putting financial strain on the insured. Nearly half of Americans with auto insurance (49%) and Americans with homeowners insurance (46%) say they’re stressed about the costs of their premiums, according to a new NerdWallet survey.

The survey, conducted online by The Harris Poll, asked over 2,000 Americans about their home and auto insurance. In addition to asking about financial stress brought on by premiums, we asked about rate hikes, the impact of severe weather on insurance costs and how Americans feel about insurance requirements.

-

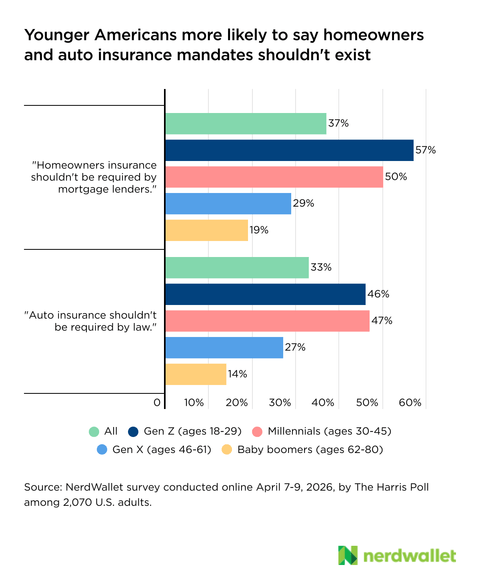

About a third of Americans (33%) say auto insurance shouldn’t be required by law and 37% of Americans say homeowners insurance shouldn’t be required by mortgage lenders.

-

Over a quarter of Americans with auto insurance (27%) say their premium increased in the past 12 months.

-

One-third of Americans with homeowners insurance (34%) say their premium increased in the past 12 months and 21% with homeowners insurance say severe weather or natural disasters have impacted rates in their area.

-

Around one-fifth of Americans with auto insurance (18%) say they have the minimum required coverage for their state and about 1 in 8 Americans with homeowners insurance (12%) have the minimum required coverage for their mortgage lender. This suggests that some Americans may be underinsured in the event of catastrophe.

“Insurance premiums have been on the rise for several years due to the increasing frequency of extreme weather events and inflation pressures,” says Kaz Weida, an insurance expert at NerdWallet. “Inflation doesn’t just affect gas and food prices. It also means it costs more to repair cars and homes, and those increased costs show up in your premium eventually. Recent rate hikes could drive some folks strapped for cash to consider trimming back or cutting coverage altogether.”

Around a third of Americans say insurance shouldn’t be required

Auto insurance is required by almost every state in the U.S. Homeowners insurance, while not legally mandated by the state or federal government, is typically required by mortgage lenders. And some Americans aren’t on board with these mandates.

About a third of Americans (33%) say auto insurance shouldn’t be required by law and 37% of Americans say homeowners insurance shouldn’t be required by mortgage lenders. These sentiments are held more strongly by younger Americans than their older counterparts.

This doesn’t mean younger Americans are better equipped to handle auto and homeowner repairs out of pocket in case of a wreck or storm damage. Instead, this may indicate that the high cost of insurance may have some people feeling that it’s worth the risk of forgoing coverage.

About 1 in 5 with auto insurance have the minimum coverage

Whether you think auto insurance should be mandated or not, it most likely is in your state, and it can be expensive.

According to the survey, more than a quarter of Americans with auto insurance (27%) say their premium increased in the past 12 months. One contributor to these rate hikes is weather — 10% of auto-insured Americans say severe weather or natural disasters have impacted auto insurance rates in their area.

Some may have taken steps to reduce costs where they can. Around one-fifth of Americans with auto insurance (18%) say they have the minimum required coverage for their state. And 6% decreased their auto insurance coverage in the past 12 months. While these actions could take some of the stress off your wallet month-to-month, they could be financially catastrophic in the case of an accident.

How to avoid underinsuring your vehicle

“When it comes to liability insurance, don’t assume just because you have the coverage your state requires, you’re in good shape if you get into an accident. Many state minimum requirements are not enough to cover the real-world costs of an accident,” Weida says.

As for collision and comprehensive coverage, these may be optional for those who own their cars outright (but likely required for those with a financed vehicle). If you can’t realistically afford to replace a totaled vehicle, it’s probably worth the additional cost.

One-fifth with homeowners insurance say weather impacted rates

If you thought auto insurance was expensive, homeowners insurance has entered the chat.

The median homeowners insurance in the U.S. isn’t much more than auto insurance — $2,490 annually, according to NerdWallet analysis of Quadrant Information Services data. But depending on your state, insuring a home could cost a lot more than insuring a car. For instance, in Kansas, the median homeowners insurance rate is $5,533, compared to the state’s median car insurance rate of $2,565.

According to the survey, a third of Americans with homeowners insurance (34%) say their premium increased in the past 12 months. Like with auto insurance, a contributing factor is weather: 21% with homeowners insurance say severe weather or natural disasters have impacted rates in their area.

Some of the most expensive states for homeowners insurance — Oklahoma, Nebraska and Kansas — are interestingly among the most affordable states for overall cost of living. They’re also in the middle of the country in the “hail belt”, which can be more costly to insure than homes in states prone to hurricanes or wildfires.

About 1 in 8 Americans with homeowners insurance (12%) have the minimum required coverage for their mortgage lender, according to the survey. And 4% of home-insured Americans decreased their coverage in the past 12 months.

How to avoid underinsuring your home

Personal liability coverage is there in case someone gets hurt on your property or you’re responsible for damage to someone else’s property. Like with auto insurance, NerdWallet recommends a liability limit high enough to protect your assets.

“The second step is to compare your personal liability limits to your current net worth. If you haven’t updated your policy in a while, you may need to adjust those liability limits to keep pace with your income and assets.”

Decreasing insurance coverage could make sense for your situation, but if it’s purely financially motivated, it could end up hurting more later if something happens to your home or vehicle. Instead, take steps to reduce costs, not coverage.

Bundle up: Nearly half of Americans with homeowners insurance (47%) say their auto insurance and homeowners insurance policies are bundled. Some insurers offer discounts for having multiple insurance policies. That said, bundling may not always be the cheapest option; even with a discount, it’s still important to shop around periodically.

Make future vehicle purchases with insurance rates in mind: Around one-fifth of Americans with auto insurance (19%) say rates would impact the type of car they choose to buy. Premiums can vary by vehicle make and model, and a luxury car could be more expensive to insure than something more basic. Keep this in mind next time you head to the car lot for a new (or new to you) vehicle.

Disclaimer

NerdWallet disclaims, expressly and impliedly, all warranties of any kind, including those of merchantability and fitness for a particular purpose or whether the article’s information is accurate, reliable or free of errors. Use or reliance on this information is at your own risk, and its completeness and accuracy are not guaranteed. The contents in this article should not be relied upon or associated with the future performance of NerdWallet or any of its affiliates or subsidiaries. Statements that are not historical facts are forward-looking statements that involve risks and uncertainties as indicated by words such as “believes,” “expects,” “estimates,” “may,” “will,” “should” or “anticipates” or similar expressions. These forward-looking statements may materially differ from NerdWallet’s presentation of information to analysts and its actual operational and financial results.