Microsoft (MSFT +0.60%) is roaring back. Since April began, the stock has jumped by more than 14% as of this writing. However, the tech leader is still down by over 20% since it hit its all-time high in October 2025. Could Microsoft maintain its recent momentum, or will ongoing developments — including inflation and geopolitical tension — drag the stock back down? It’s hard to predict what will happen in the next few months. But for investors focused on the long game, there are excellent reasons to think it’s still time to buy the dip. Here are three of them.

Image source: The Motley Fool.

1. AI won’t replace Microsoft

One reason some investors are worried about Microsoft’s prospects is that they believe the company’s services will be replaced by artificial intelligence (AI). It’s not just Microsoft either. Many software stocks have been struggling for this very reason. However, how likely is it that AI will actually make Microsoft’s products obsolete? Once upon a time, some people feared the same would happen to Alphabet.

They thought AI chatbots would disrupt the company’s search empire, which it practically holds a monopoly over. Since Alphabet generates the lion’s share of its revenue from search-related advertising, that would have been a significant blow to the business.

Except, things didn’t unfold that way at all. Alphabet adapted, incorporated AI into its search capabilities, and, if anything, the technology improved the company’s business. Now, there are many differences between Microsoft and Alphabet. Just because the latter adapted doesn’t mean the former will, too. Even so, Microsoft has a deep culture of innovation and large, established relationships with enterprises.

Those two advantages can allow the company to get ahead of the threat posed by AI, update its services with that in mind, and maintain a solid share of its core markets. Microsoft has already started doing that. The company’s Copilot is an AI assistant integrated across its productivity suite. The tech giant will likely continue finding new ways to keep the AI threat at bay. In my view, it will be successful.

Today’s Change

(0.60%) $2.53

Current Price

$422.79

Key Data Points

Market Cap

$3.1T

Day’s Range

$420.69 – $431.58

52wk Range

$355.67 – $555.45

Volume

49M

Avg Vol

38M

Gross Margin

68.59%

Dividend Yield

0.82%

2. Microsoft can endure downturns

Investors worried about inflation or a potential recession should seriously consider Microsoft. It may be a tech stock that’s fairly volatile compared to many corporations in more defensive industries, but several aspects of its business should allow it to navigate economic downturns much better than many of its peers. Consider, for instance, that a significant portion of Microsoft’s revenue comes from subscriptions, including from individuals, businesses of all sizes, and even government or non-profit institutions.

That grants the company a large base of recurring revenue, much of which should remain intact even in a recession. Further, Microsoft arguably benefits from pricing power, enabling it to pass some of the cost increases to its customers without a significant exodus. Microsoft is also a great dividend stock. The company has increased its payouts by almost 153% over the past 10 years. This is relevant because if economic troubles lead to a market crash, regular dividends can help smooth out market losses. And we have little reason to believe Microsoft would suspend its payouts.

The company’s underlying business is rock solid, backed by an AAA rating — the highest available — from S&P Global, along with significant free cash flow and a highly conservative cash payout ratio of 33.6%. All that makes Microsoft a great stock to buy now.

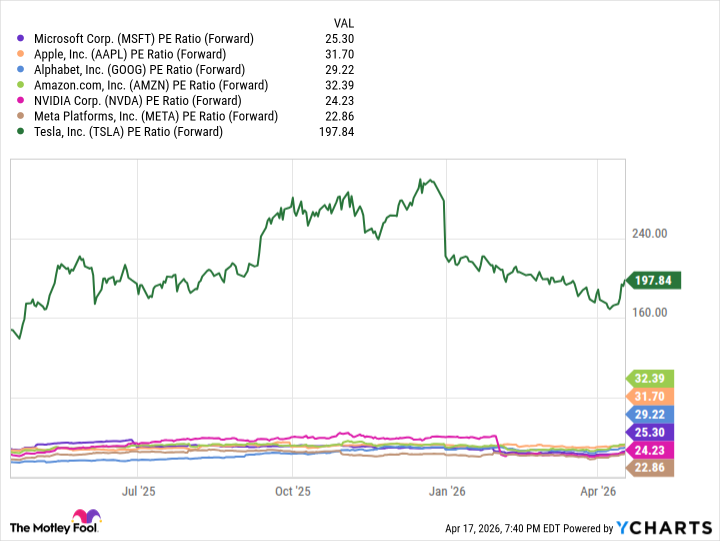

3. The price is (still) right

Even after its run over the past two weeks, Microsoft’s shares remain reasonably valued when compared to its Magnificent Seven peers.

MSFT PE Ratio (Forward) data by YCharts

Microsoft isn’t the cheapest in this group based on its forward price-to-earnings (P/E), but it certainly isn’t the most expensive either. Even putting aside the outlier, Tesla, Microsoft’s forward P/E is lower than the average of the remaining six right now. Microsoft may or may not maintain the recent momentum in the next few months, but the company’s long-term prospects remain attractive. And those who purchase its shares at current levels will likely be glad they did so in 10 years.