The pharmaceutical sector has a reputation for offering high-growth opportunities, but is also known for being risky. However, there’s more to that sector than meets the eye.

There are pharmaceutical companies that can fit into a value investor’s portfolio. Broadly speaking, these companies look undervalued, with high dividend yields and the ability to generate steady revenue.

A company that checks all three of those boxes at this moment is Bristol Myers Squibb (BMY 1.48%).

Image source: Getty Images.

Why Bristol Myers Squibb looks like a value stock

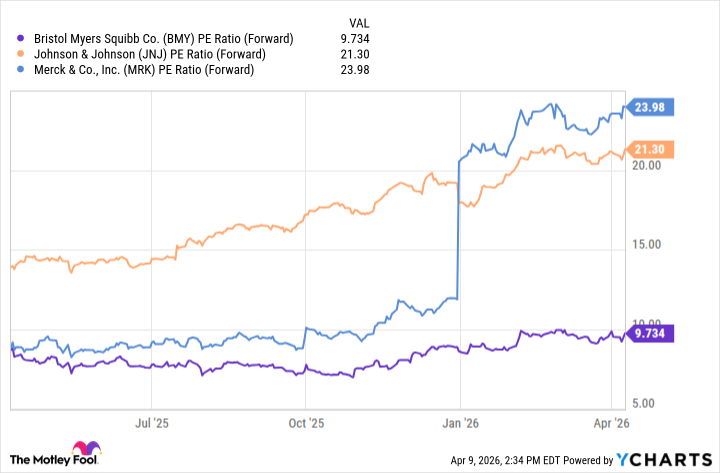

Bristol’s forward price-to-earnings (P/E) ratio — based on estimates for earnings — is around 9.5, which makes it look like a bargain compared to some other pharmaceutical stocks. For example, Johnson & Johnson has a forward P/E ratio of 21, while Merck‘s is 24.

BMY PE Ratio (Forward) data by YCharts

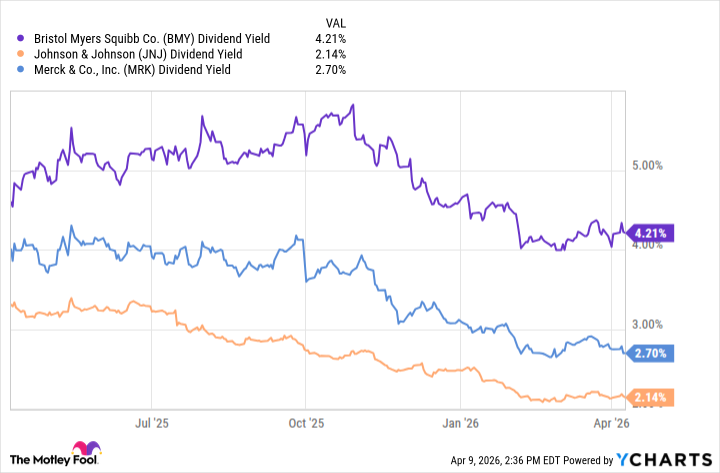

Bristol Myers Squibb’s dividend yield is an enticing 4.2%, which is notably higher than those competitors’ yields. It has also increased its dividend payout for 17 consecutive years and has paid a dividend for 94 consecutive years.

BMY Dividend Yield data by YCharts

In 2024, Bristol Myers Squibb reported $48.3 billion in revenue, followed by $48.2 billion in 2025. For 2026, Bristol expects revenue to fall between $46 billion and $47.5 billion. The slowing revenue is something to take note of, but what’s also worth noting is that the 2026 outlook is still fairly similar to previous years, highlighting Bristol’s consistency.

Today’s Change

(-1.48%) $-0.88

Current Price

$58.59

Key Data Points

Market Cap

$119B

Day’s Range

$58.47 – $59.78

52wk Range

$42.52 – $62.89

Volume

232K

Avg Vol

13M

Gross Margin

65.89%

Dividend Yield

4.26%

Just looking at the forward P/E, dividend yield, and stable revenue, on the surface, this seems like a strong value investment. Still, it’s always important to ask: Why does this opportunity exist? What is the rest of the market missing?

What the rest of the market is worried about is slowing legacy revenue, patent cliffs, and acquisition costs.

The challenges that created a favorable valuation

In 2024, Bristol reported revenue of $25.7 billion from its “legacy portfolio,” which fell sharply to $21.8 billion in 2025.

Eliquis, a blood thinner drug in that legacy portfolio that generated $14.4 billion in sales in 2025, faces an upcoming patent cliff. That’s worrisome.

Some investors are also worried about Bristol’s agreement to acquire Orbital Therapeutics for $1.5 billion, as the company is already sitting on more than $47 billion in debt.

When you add it all up, it’s no surprise that the forward P/E suggests future expectations are low compared to those of similar pharmaceutical stocks.

Those are all very real concerns, so the next step to see whether Bristol is truly a value is to explore how it’s addressing them.

Getting over the hurdles holding back the stock

Just as a quick refresher: Bristol’s legacy portfolio dropped from $25.7 billion in revenue in 2024 to $21.8 billion in revenue in 2025.

The good news for current shareholders or anyone considering investing is that revenue from its “growth portfolio” is, well, growing. Revenue for the growth portfolio jumped from $22.6 billion in 2024 to $26.4 billion in 2025.

That growth portfolio featured several drugs with worldwide sales of $1 billion or more.

The potential acquisition of Orbital Therapeutics isn’t cheap, but it could help Bristol build out its pipeline, which could help address the revenue lost from upcoming patent cliffs. Orbital is developing RNA medicines for the treatment of autoimmune diseases. Consulting firm Towards Healthcare projects that the global RNA therapeutics and vaccine market will reach over $205 billion by 2035.

“Our core business is strong and growing, and we have the potential to achieve industry-leading, sustainable growth into the 2030s and beyond,” Bristol CEO Christopher Boerner said in the company’s press release for its Q4 2025 and full-year 2025 results.

If things work out as planned, Bristol could be a true value at today’s price.