The easiest stocks to own are the ones that pay you growing dividends every year. Dividend income lets you sit back and appreciate a steady cash stream coming to your portfolio, regardless of where a stock trades in the interim.

Growing dividend payouts are the best stocks to own with this strategy for those with a longer time horizon, even if their current dividend yields aren’t high.

But how do you determine what stocks have the best dividend growth potential? It all comes down to earnings growth. Here are two dividend stocks worth buying more of, even at today’s prices.

Image source: Getty Images.

Betting on new age nicotine

Tobacco use is declining worldwide. But nicotine usage is not. Non-tobacco nicotine products are growing faster than the decline of traditional cigarettes, with new products like electronic vaping and pouches bringing the category back to growth.

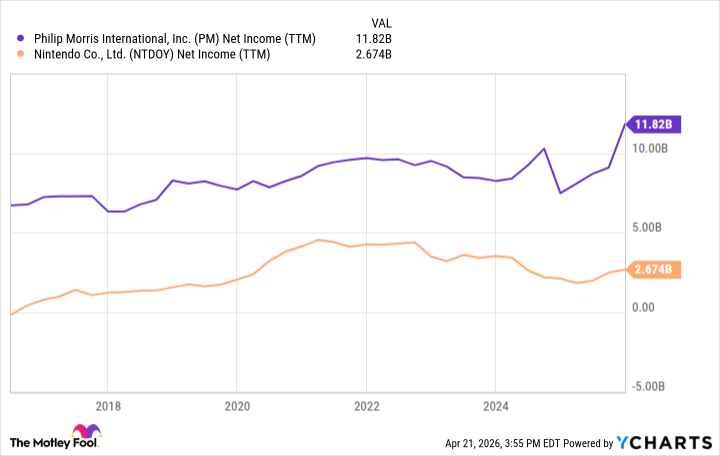

No company has benefited more from this transition than Philip Morris International (PM 2.95%). The tobacco giant generated $16.9 billion in revenue from its smoke-free business in 2025, up 15% year over year, and now accounts for more than 40% of overall sales. Brands such as Zyn in nicotine pouches and Iqos in heat-not-burn smoking devices are growing quickly around the globe in wealthier markets like the United States, Europe, and Japan.

Right now, Philip Morris stock is down 18.5% from all-time highs, sporting a starting dividend yield of 3.8%. As the company’s new-age nicotine products continue to grow, its record-high operating income of $14.4 billion last year will keep rising. This will fuel dividend growth, as the stock’s dividend has risen 44% cumulatively over the last 10 years. Philip Morris International is a great dividend growth stock at today’s prices.

Philip Morris International

Today’s Change

(-2.95%) $-4.99

Current Price

$164.20

Key Data Points

Market Cap

$256B

Day’s Range

$162.92 – $168.16

52wk Range

$142.11 – $191.30

Volume

5.1M

Avg Vol

5.3M

Gross Margin

69.74%

Dividend Yield

3.51%

An incoming profit inflection

Nintendo (NTDOY 2.93%) is undergoing an even larger business transition compared to Philip Morris International. It is currently transitioning its player base to its new Nintendo gaming hardware, the Nintendo Switch 2, which was released less than a year ago. The device is projected to have sold 19 million units through the end of Nintendo’s fiscal year, which ended in March.

The stock’s current dividend yield is 2.1%, which is below the desired level. However, investors can use management’s 60% dividend payout policy as a barometer for where dividends might grow in the years ahead.

At the start of a hardware cycle, Nintendo will sell many new units but generate little profit growth due to the slim margins on hardware sales. Software or game sales are where it makes its money, and those sales will follow in the years ahead. We are already seeing this boost with new games like Pokémon Pokopia, which sold 2.2 million units in its first four days after release.

Today’s Change

(-2.93%) $-0.38

Current Price

$12.41

Key Data Points

Market Cap

$57B

Day’s Range

$12.32 – $12.47

52wk Range

$12.32 – $24.92

Volume

2.8M

Avg Vol

3.1M

Gross Margin

40.42%

Dividend Yield

0.35%

Along with Nintendo’s foray into other entertainment initiatives such as theme parks and movies, investors should see net profit inflect higher over the next five years. Nintendo’s net income was $4 billion in 2021. With inflation, higher selling prices, and revenue diversification, I think Nintendo can clear well over $5 billion in net profit in the years ahead, leaving $3 billion a year for dividend payouts.

The stock currently has a market cap of $61 billion and a large cash balance on the balance sheet. This will give Nintendo a forecasted dividend yield of 5% over the next few years based on its payout policy of 60% of net income.

PM Net Income (TTM) data by YCharts.

Why starting dividend yield isn’t everything

Novice investors will look at high starting dividend yields and think they are the best dividend stocks to buy. These are dangerous stocks to buy, because it typically means the businesses are in distress and are liable to cut dividends in the future. A better hunting ground is great businesses with the potential for durable dividend growth in the years ahead.

Both Philip Morris and Nintendo are great businesses that have stood the test of time. At today’s prices, they look like fantastic dividend growth stocks you can sit and watch the cash roll in from for years to come.