Most people wouldn’t place Amazon (AMZN +0.26%) and Nvidia (NVDA +1.67%) in the same competitive landscape. At a glance, Amazon looks like an e-commerce investment, while Nvidia is a bet on a continued artificial intelligence (AI) infrastructure build-out. However, that’s only partially true.

Amazon has a booming cloud computing wing with Amazon Web Services (AWS). While it has Nvidia chips to support training and inference, it also has its own custom AI chips, whose business is on fire. Amazon took several shots at Nvidia in its recent shareholder letter, showcasing the dominance of Amazon’s custom AI chips over Nvidia’s, so much so that some investors may be worried about Nvidia losing significant market share to Amazon.

So, is Amazon now the stock to buy over Nvidia? Let’s find out.

Image source: Getty Images.

Amazon’s chips showcase better performance

In Amazon’s recent shareholder letter, it disclosed several impressive stats about Amazon’s custom chips. They started by discussing its first custom chips, Graviton.

Before 2018, Intel CPUs dominated the cloud computing space. However, after Amazon introduced Graviton, its custom CPU, it quickly took over by offering a 40% better price performance than Intel’s chips. Amazon predicts that the AI market will go the same way.

Today’s Change

(0.26%) $0.66

Current Price

$250.36

Key Data Points

Market Cap

$2.7T

Day’s Range

$250.11 – $256.19

52wk Range

$165.28 – $258.60

Volume

2.3M

Avg Vol

52M

Gross Margin

50.29%

Its Trainium2 chip offers 30% better price performance than GPUs, and its capacity is nearly sold out. The next generation, Trainium3, which just entered work at the start of this year, has even better performance and is also nearly fully accounted for. Trainium4, which is 18 months from entering service, is also nearly sold out. Clearly, if Amazon could increase its production capacity, it could steal more market share from standard GPU-based training.

However, Amazon isn’t walking away from Nvidia, either. It also noted that it will continue to make Amazon the best place to run Nvidia chips.

Why? Easy. Nvidia’s production capacity is far greater than Amazon’s, so it needs to maintain a great relationship with Nvidia; otherwise, it could suffer from a lack of resources and lose clients to competitors.

Another reason why Amazon must keep Nvidia’s chips around is that some clients would rather use Nvidia’s products. While Trainium chips may offer better price performance, that’s not everything. If a single client uses Amazon’s Trainium chips exclusively, Amazon can raise prices to unreasonable levels.

Because the client’s workload is locked into a custom chip architecture, it makes it impossible to switch, so the client must pay Amazon what they want. If they run their workloads on Nvidia’s architecture, they can switch to another cloud provider’s services or build their own data center using the same chip family. I’m not saying these options are cheap or easy, but customers have that freedom.

Today’s Change

(1.67%) $3.32

Current Price

$201.67

Key Data Points

Market Cap

$4.9T

Day’s Range

$199.28 – $201.68

52wk Range

$95.04 – $212.19

Volume

5M

Avg Vol

177M

Gross Margin

71.07%

Dividend Yield

0.02%

So, is it the end of the world for Nvidia that Amazon is producing chips with better bang-for-the-buck performance? I don’t think so. This competition keeps Nvidia innovative and ensures that it doesn’t rest on past success.

Nvidia investors need to be aware of the situation, as they must understand that if growth rates fall, it may not be because the AI build-out is slowing; it just could be losing market share. However, we’ve seen no such signs so far.

Nvidia’s growth rates are still accelerating

The reality is, there is so much demand for AI computing power that AI hyperscalers are willing to take whatever increased capacity that they can get their hands on, be it custom Amazon chips or Nvidia’s.

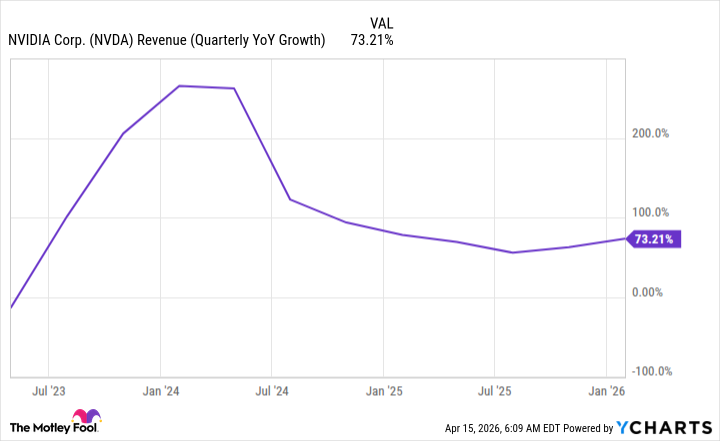

This trend results in accelerating growth rates for Nvidia. In Q4, its growth rate was 73%. In Q1 and Q2, Wall Street analysts estimate 79% and 85% growth. That’s downright incredible and displays Nvidia’s strength.

NVDA Revenue (Quarterly YoY Growth) data by YCharts

I think Nvidia will be OK over the long term, and the future is likely a combination of custom chips and Nvidia’s more commoditized hardware. We’re already seeing this from one of the leading generative AI companies, Anthropic, which trains its model on a mix of chips, including Nvidia’s, Amazon’s custom chips, and Alphabet company Google’s custom chips. That will likely be the path many companies take, leading to multiple winners in the AI chip space.

So this isn’t exactly checkmate, but a sign of healthy competition.