Micron Technology (MU +5.07%) stock has delivered outstanding gains to investors so far in 2026, with shares of the memory specialist rising by 208% as of this writing, and the good part is that the stock could get a big shot in the arm in June.

Micron is set to release its fiscal 2026 third-quarter results on June 24. The favorable demand-supply conditions in the memory market, driven by artificial intelligence (AI) data centers, are likely to help Micron deliver another solid set of results. Consensus estimates are projecting a whopping 261% increase in the company’s revenue for fiscal Q3, along with a 10x increase in earnings.

So, don’t be surprised to see Micron stock getting a nice shot in the arm following its upcoming report in June, especially considering that it trades at a really attractive valuation. However, there’s another high-flying company that’s set to release its quarterly report on June 4 — Ciena (CIEN +1.76%). Its shares have jumped by 136% in 2026, and the incredible growth that it has been delivering could give it a nice boost next month.

Let’s see why Ciena is my top AI stock to buy in June, even after the stunning gains it has delivered so far this year.

Image source: The Motley Fool.

Like Micron, Ciena is an important player in the AI infrastructure ecosystem

Micron’s high-bandwidth memory (HBM) chips help AI data centers overcome a key bottleneck. These specialized memory chips continuously feed large datasets to AI processors quickly and power-efficiently, thereby reducing latency and enabling AI model training and inference applications to run seamlessly.

The faster data access enabled by HBM means AI processors in data centers won’t need to sit idle and waste resources. Ciena’s optical networking components also help address this bottleneck by enabling high-speed data transfer in AI data center clusters. The massive size of AI models means that multiple AI data centers and servers need to be linked together through high-speed networks.

Today’s Change

(1.76%) $10.05

Current Price

$580.23

Key Data Points

Market Cap

$82B

Day’s Range

$539.57 – $582.47

52wk Range

$70.77 – $605.61

Volume

3.9M

Avg Vol

2.7M

Gross Margin

39.48%

Ciena’s optical components power these data center interconnects (DCI). Precedence Research estimates that the global data center interconnect market could grow from just under $19 billion this year to almost $65 billion in 2035, at an annual rate of almost 15%. Meanwhile, the demand for optical networking components could increase at a compound annual growth rate (CAGR) of 21% over the next five years to support fast connections in AI data centers, according to market research provider Cignal AI.

This explains why Ciena has been growing at an incredible pace. The company’s revenue increased by 33% year over year in the first quarter of fiscal 2026 (which ended on Jan. 31, 2026) to $1.43 billion. The company anticipates full-year revenue to increase by 28% to $6.1 billion at the midpoint of its guidance range, an improvement over the 19% growth it clocked in the previous fiscal year.

What’s more, the AI data center-fueled demand is leading to higher profitability for Ciena. Its adjusted earnings increased by 111% year over year in fiscal Q1. The good part is that the strong pricing power it enjoys in the optical transport industry is expected to drive further margin gains in the second half of the fiscal year. Ciena notes that demand for its products is outpacing supply, leading to a jump in prices.

In fact, the company expects demand to be higher than supply “at least for the next several quarters,” suggesting that further price increments could be in the cards. Another important point is that Ciena received $2 billion in orders in fiscal Q1, exceeding its revenue. The company ended the quarter with an order backlog of $7 billion.

So, don’t be surprised to see Ciena’s revenue and earnings growth landing ahead of expectations when it releases fiscal Q2 results on June 4.

The stock is expensive, but investors shouldn’t miss the bigger picture

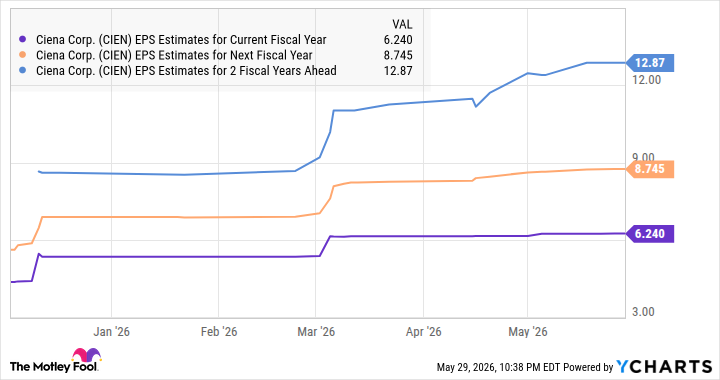

Ciena is trading at a whopping 372 times trailing earnings. However, its forward earnings multiple of 128 points toward a big jump in its earnings. Of course, Ciena’s forward earnings multiple is also on the expensive side. However, its premium can be justified by a potential 136% increase in its earnings this fiscal year, according to Yahoo! Finance.

Moreover, the supply constraints in the optical networking market that Ciena expects in the coming quarters explain why analysts are expecting its bottom-line growth to accelerate.

Data by YCharts

Don’t be surprised to see Ciena sustaining its healthy earnings growth rate beyond the next three fiscal years. That’s because massive investments in AI data centers are poised to continue through the end of the decade, with McKinsey expecting a whopping $5.2 trillion in annual capital spending in 2030. As Ciena provides key components that help AI data centers operate smoothly, it is likely to continue to witness robust top- and bottom-line growth over the long run.

So, growth-oriented investors can still consider buying Ciena stock ahead of its earnings report, as its terrific earnings power should drive more upside.