Artificial intelligence (AI) infrastructure spending has rocketed higher in recent years. Importantly, there are no signs of a slowdown in AI infrastructure spending.

This is great news for Micron Technology (MU +5.07%), which provides a critical component that helps chips used for running AI applications unlock their full potential. In fact, a recent report suggests that massive investments in AI data centers will get even bigger in 2026. This is your signal to buy Micron stock, as the memory specialist is the direct beneficiary of a spike in AI infrastructure spending.

Let’s look at the reasons why.

Image source: Micron Technology.

The increasing data center capex will be a tailwind for Micron Technology

Market research firm TrendForce substantially raised its 2026 capital expenditure forecast by the world’s top nine cloud service providers (CSPs) this month. The firm expects a 79% jump in capex by CSPs this year, up from the earlier estimate of a 61% improvement.

Today’s Change

(5.07%) $46.82

Current Price

$970.34

Key Data Points

Market Cap

$1.1T

Day’s Range

$940.59 – $981.21

52wk Range

$94.40 – $981.21

Volume

1.8M

Avg Vol

47.8M

Gross Margin

58.54%

Dividend Yield

0.05%

The overall capex will come in at a whopping $830 billion, and growth in this metric will exceed the 79% increase seen last year. TrendForce notes that the capex will mostly be allocated toward developing GPU (graphics processing unit) clusters and custom AI processors.

Both these chips are equipped with more high-bandwidth memory (HBM) to ensure they can be fed massive datasets quickly and don’t sit idle, thereby reducing downtime associated with running AI workloads. For instance, the demand for HBM used in custom AI processors is expected to jump by 35x between 2024 and 2028, according to Counterpoint Research.

Meanwhile, Nvidia’s move to equip its latest Vera Rubin GPU with 288 gigabytes (GB) of HBM, as compared to the 80GB HBM on the highly popular H100 GPU that was launched in 2022, makes it clear that Micron’s memory chips are going to witness a solid spike in demand as data center capex rises.

As HBM requires thrice the wafer capacity of conventional memory chips, the ongoing shortage prevailing in the memory industry is likely to continue. This presents an ideal situation for Micron, which has been experiencing red-hot revenue and earnings growth owing to tight memory supply.

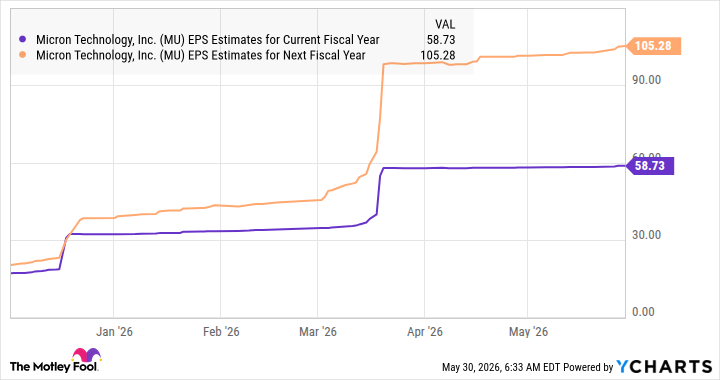

Micron’s earnings growth potential suggests that the stock is set to go parabolic

Micron stock has shot up by 903% over the past year, taking its market cap past the $1 trillion mark. However, the acceleration in AI data center capex means that it isn’t done soaring yet.

As a tight memory supply is likely to persist at least until 2028, Micron will continue to benefit from a favorable pricing environment. Not surprisingly, its earnings are expected to soar in fiscal 2027 (which will end in August next year).

Data by YCharts

If Micron trades at even 30 times earnings after a year (a discount to the Nasdaq Composite‘s earnings multiple of 42.5), its stock price could jump to $3,158, based on the earnings it is poised to deliver next fiscal year. That’s 3.2x Micron’s current stock price, which is why investors should consider buying this AI stock before it rips higher.