Wall Street analysts have to answer to their bosses every day, which can make it hard to take a long-term view of a business. How do you justify a buy rating on a company when its stock is underperforming, and its business is struggling? That’s the quandary that analysts face today with Pfizer (PFE +0.19%).

There are 29 analysts with ratings on the company. Only 2 have it as a strong buy, with another nine at buy. The rest have Pfizer at a hold, underperform, or sell. In other words, the overall Wall Street perception of the company is negative, with more than 60% suggesting investors take a cautious view of the highly respected drug company. Contrarian investors should see this as a sign to consider buying the stock.

Image source: Getty Images.

There is a lot to dislike about Pfizer today

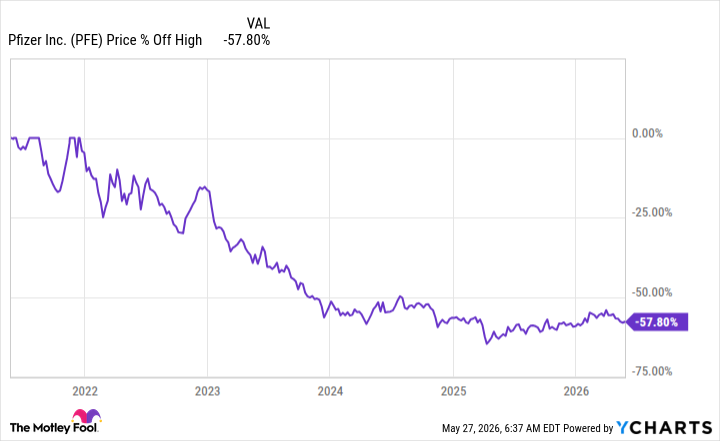

Pfizer’s stock has fallen more than 50% from its 2021 high. Investors are clearly downbeat on the business. That’s just one piece of evidence that the broadly negative view of the drug maker among Wall Street analysts isn’t unfounded. In fact, it is fairly easy to justify the negativity here.

For example, Pfizer has several important drugs that will lose patent protection between now and 2028. The 2028 patent expirations for Eliquis and Vyndaqel, two cardiology drugs, are likely to be a particular hit to the company’s top and bottom lines. Pfizer is working on new drugs to fill the gap, but drug development doesn’t work on a set timeline.

That was on clear display when Pfizer had to drop its internally developed GLP-1 drug in the first half of 2025. GLP-1 weight-loss drugs are a new category in the industry that has seen huge demand. Not having a product here is a major problem from both a business perspective and an investor perception standpoint.

Pfizer hasn’t suddenly become a bad company

The negative view of Pfizer today has pushed its dividend yield up 6.6%, well above the market’s 1.1% and the average drug maker’s 1.7%. The payout ratio is over 100% right now, but the company continues to say it will support the dividend. Notably, the company can use debt and cash to maintain the payment while it works through a difficult period.

And it is working through this difficult period, even if the results aren’t yet obvious on the top and bottom lines. For example, shortly after dropping its own GLP-1 drug, it bought a company with a more compelling GLP-1 candidate, which it is now focused on developing. Meanwhile, Pfizer continues to push forward with new vaccines, migraine medications, and oncology drugs.

Today’s Change

(0.19%) $0.05

Current Price

$26.19

Key Data Points

Market Cap

$149B

Day’s Range

$25.93 – $26.22

52wk Range

$23.06 – $28.75

Volume

798.7K

Avg Vol

37.4M

Gross Margin

65.16%

Dividend Yield

6.57%

This isn’t a company that has simply given up. It is a company that is working just as hard as it always has. The problem is simply a mismatch between patent expirations and the pace of new drug development. That’s not unusual in the drug space, but short-term-focused investors and Wall Street analysts aren’t willing to give Pfizer the benefit of the doubt and think beyond the current headwinds.

Pfizer is a respected company and will get back on its feet

For the most part, Wall Street analysts and investors seem to be focused on Pfizer’s recent weak performance. That’s understandable, but it ignores the company’s long and successful history. If you are willing to go against the grain, you can collect a large yield while you wait for Pfizer to get back on track. And history suggests it will eventually do just that. If you think long term, Wall Street is likely dead wrong on this drug giant.