It’s been a history-making month in more ways than one for Wall Street. We’ve witnessed the Dow Jones Industrial Average (^DJI +0.72%), S&P 500 (^GSPC +0.22%), and Nasdaq Composite (^IXIC +0.20%) all romp to record-closing highs. We also observed a rare changing of the guard at America’s foremost financial institution, the Federal Reserve.

May 15 was the final day of Jerome Powell’s second term as Fed chair. His final year was marked by harsh criticism from President Donald Trump over interest rates and the Federal Open Market Committee’s (FOMC) lack of action in slashing the federal funds target rate. The FOMC is the 12-person body, including the Fed chair, responsible for setting the nation’s monetary policy.

Kevin Warsh was sworn in as the new Fed chair on May 22. Image source: Official White House Photo by Daniel Torok.

Trump’s handpicked successor to Jerome Powell is Kevin Warsh. Warsh previously served on the FOMC from Feb. 24, 2006, to March 31, 2011, and played an instrumental role in steering the U.S. economy through the financial crisis with the other 11 voting members.

But none of Warsh’s prior experience can prepare him for the Federal Reserve’s nightmare scenario: stagflation.

The puzzle pieces for stagflation are firmly in place

Stagflation is characterized by high unemployment, stagnant or declining economic growth, and high inflation. It’s arguably the most challenging situation for the central bank to combat, given that there’s no blueprint to quickly fix it.

If the FOMC lowers interest rates to spur economic growth and hiring, it risks inflation rising further. On the other hand, hiking interest rates can help stabilize prices at the detriment of hiring and/or economic growth. There’s no easy fix.

All three variables of stagflation are currently present or expected, based on historical precedent.

The trailing 12-month (TTM) inflation rate recently hit a three-year high, courtesy of two decisions made by President Trump. First, his decision to implement sweeping global tariffs has been modestly inflationary. Adding duties to unfinished imported goods can increase production expenses for U.S. companies, leading to higher costs for consumers.

There is a near-perfect correlation between US oil prices and US CPI inflation, as shown in our below analysis.

Oil prices have averaged near $100/barrel since March 6th, or 79 days.

The longer this persists, the more inflation we will see.

Asset owners are the only winners. pic.twitter.com/phpkZteX1l

— The Kobeissi Letter (@KobeissiLetter) May 24, 2026

The Iran war is the source of the secondary price shock. Shortly after Trump gave the order for the U.S. military to attack Iran on Feb. 28, the latter shut the Strait of Hormuz to virtually all commercial traffic, thereby halting the flow of approximately 20 million barrels of petroleum liquids per day. Crude oil prices and fuel prices have skyrocketed in the wake of the largest energy supply disruption in modern history.

Between February and April, TTM inflation has surged from 2.4% to 3.8%, and Trumpflation isn’t close to peaking. The inflationary effects of energy price shocks on businesses often lag a few months. Once these impacts are accounted for in economic data, inflation can push higher.

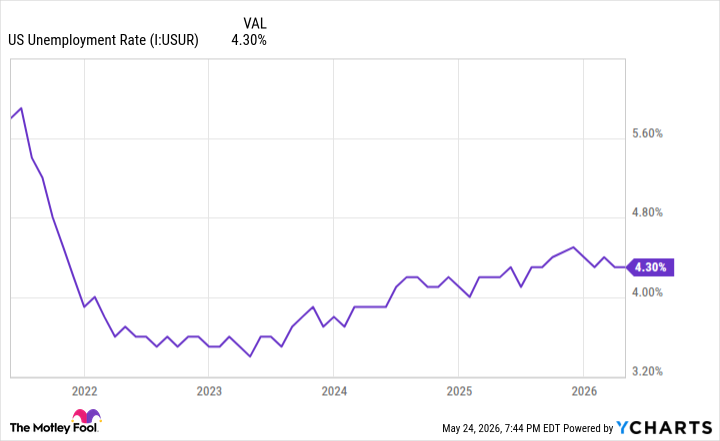

US Unemployment Rate data by YCharts.

The unemployment rate is also expected to be an issue. Though the 4.3% unemployment rate reported in April is historically low, unemployment has been modestly trending up for the last three years (3.4% in April 2023). History tells us that crude oil price shocks almost always lead to job losses as businesses cope with rising transportation and production costs.

The final piece of the stagflation puzzle is stagnant or declining gross domestic product (GDP). Since Trump took office, annualized U.S. GDP has clocked in at (0.6%), 3.8%, 4.4%, 0.5%, and 2%, respectively, over five quarters. On average, quarterly annualized GDP growth has been just 2% since the start of 2025.

Similar to the unemployment rate, crude oil price shocks often have lasting negative impacts on economic growth.

Image source: Getty Images.

Kevin Warsh takes the reins amid a no-win scenario

Suffice it to say, Trump’s handpicked Fed chair has taken the baton from Powell amid an extraordinarily challenging period for the central bank, U.S. economy, and stock market. Something is likely to break — the question is: Will it be the Fed’s credibility, the economy, or Wall Street?

Although Warsh repeatedly talked up the central bank’s independence in his testimony before the Senate Banking Committee in April, it’s unlikely that Donald Trump’s calls for significant interest rate cuts are going to stop anytime soon. However, Warsh is caught in a no-win scenario.

If Warsh and other members of the FOMC are effectively viewed as relenting to the president’s repeated calls for lower interest rates, the central bank will lose the perception of independence, and its credibility will be thrown out the window. While lower interest rates would likely appease the stock market over the short term, the loss of credibility for a pillar of Wall Street would be damaging over the long run.

BREAKING: Newly released Fed meeting minutes show that the “majority” of officials thought rate hikes may be needed if inflation persists.

In a sudden turn of events, it appears that the market and the Fed are bracing for potential rate hikes.

— The Kobeissi Letter (@KobeissiLetter) May 20, 2026

On the other hand, if the new Fed chair and other members of the FOMC shift away from the Fed’s easing bias and raise rates in late 2026/early 2027, they’d be favoring price stability, but risking economic and Wall Street turbulence in the process. Not to mention, Warsh risks being publicly raked over the coals by Trump.

The stock market is within a stone’s throw of its priciest valuation since January 1871, according to the S&P 500’s Shiller Price-to-Earnings Ratio. Investors have been pricing in several rate cuts for 2026-2027, with lower borrowing costs expected to fuel the artificial intelligence data center build-out. Rate hikes, or even a rate-hiking bias, can pull the rug out from beneath the Dow, S&P 500, and Nasdaq Composite.

Higher interest rates can also stymie economic growth. Increasing lending costs can discourage hiring and innovation during a period of mediocre GDP growth.

Kevin Warsh and the FOMC can’t appease everyone. It’s just a matter of what eventually pays the price.