Stanley Druckenmiller’s moves have been particularly telling throughout the artificial intelligence (AI) revolution. After initiating a position in Nvidia (NVDA 1.86%) during the early generative AI surge, the billionaire money manager fully exited the position by late 2024.

During the first quarter of 2026, his Duquesne Family Office initiated new stakes in Broadcom (AVGO +0.01%), Intel (INTC +1.13%), and Arm Holdings (ARM +2.78%). This is no random reshuffling. These decisions reflect a deliberate bet that a new layer within the AI chip stack is emerging — moving away from Nvidia’s general-purpose training GPUs (graphic processing units) and shifting toward greater adoption of custom silicon and central processing units (CPUs).

Image source: Getty Images.

Why did Stanley Druckenmiller sell Nvidia stock?

Druckenmiller bought 582,915 shares of Nvidia during the fourth quarter of 2022. During the quarters that followed, he traded around Nvidia as the rise of ChatGPT sparked an AI frenzy featuring the chipmaker’s indispensable GPUs.

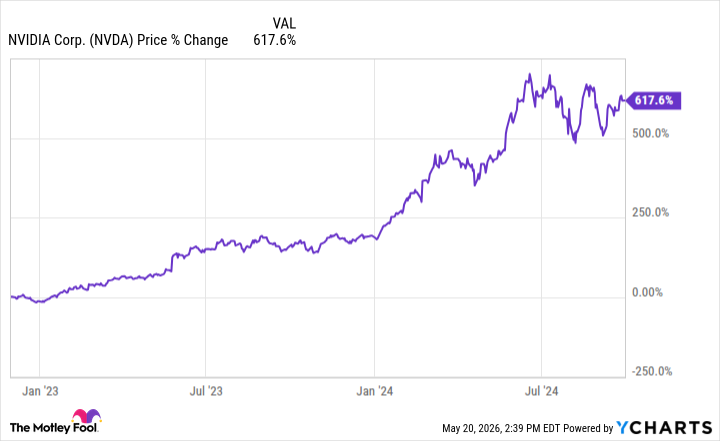

Between ChatGPT’s commercial launch (Nov. 30, 2022) and the end of the third quarter of 2024, Nvidia stock had risen more than 600%, eventually becoming the world’s most valuable company.

Even to a bull like Druckenmiller, this appeared as a clear example of extreme valuation expansion. Liquidating his position was a prudent demonstration of portfolio management: Take profits when prices get ahead of fundamentals, even in a compelling story stock such as Nvidia.

Druckenmiller said selling Nvidia was a mistake

During an interview with Bloomberg in October 2024, Druckenmiller admitted that he sold Nvidia too early — saying the move was a “big mistake.” He praised Nvidia and alluded that his fund would consider buying the stock again if the valuation became reasonable.

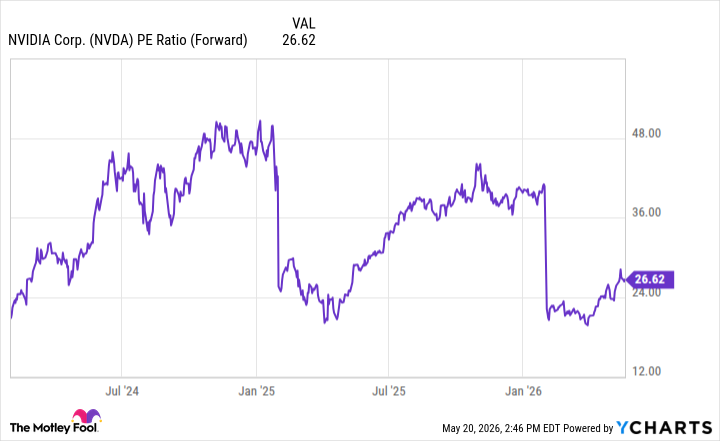

NVDA PE Ratio (Forward) data by YCharts

Nevertheless, by mid-2026, Nvidia’s valuation profile had moderated from its peaks, yet Druckenmiller still remained on the sidelines. Instead of returning to the GPU leader, he appears to be shifting capital into alternative silicon architectures positioned for what could be the next leg of the AI infrastructure boom.

The inference era is here

According to Duquesne’s Q1 13F, the fund bought 195,955 shares of Broadcom, 411,400 shares of Intel, and 106,700 shares of Arm. I see this as a signal of Druckenmiller’s conviction that inference, not training, will drive the bulk of AI compute spending in the years ahead.

Today’s Change

(1.13%) $1.34

Current Price

$119.84

Key Data Points

Market Cap

$602B

Day’s Range

$118.09 – $122.78

52wk Range

$18.96 – $132.75

Volume

82.7M

Avg Vol

117.1M

Gross Margin

35.90%

Training large language models (LLMs) is a one-time task suited for Nvidia’s GPUs. However, inference means running these models for users in real time to make predictions and estimates, thereby demanding something different: greater power efficiency, lower cost per query, and customization for specific workloads.

Hyperscalers and AI labs are responding by designing their own custom silicon chips and leaning into optimized CPU architectures. These chips consume less energy and cost less than general-purpose GPUs when performing inference at scale.

The shift away from GPUs is already becoming visible in multibillion-dollar commitments from Alphabet, Meta Platforms, Amazon, Microsoft, OpenAI, and Anthropic. Broadcom is the leader in this wave of custom application specific integrated circuits (ASICs). The company partners with some of the biggest cloud infrastructure providers, such as Google Cloud, to co-design and manufacture its specialized accelerators — known as tensor processing units (TPUs).

Intel is undergoing a renaissance as inference workloads increasingly run on traditional processors and hybrid systems. The company’s Xeon 6 and x86 CPUs are quietly becoming the backbone of enterprise data centers, including those managed by Alphabet and Nvidia.

Meanwhile, Arm supplies efficient core architectures that power custom chip designs and data center CPUs. The company’s licensing model allows chipmakers and cloud platforms to build low-power, high-bandwidth solutions ideal for inference.

Taken together, these three holdings give Druckenmiller vast exposure to the pick-and-shovel players who will profit as AI development transitions from the training phase to the realities surrounding high-volume model deployment.

Was Druckenmiller’s move savvy? I think so. These moves clearly indicate that Druckenmiller is not abandoning the AI trade. He is simply repositioning beyond the obvious macro winners. Within the infrastructure layer, he appears to be betting that custom silicon and CPUs will prove to be durable alternatives to GPUs as big tech continues to pour vast amounts of capital into inference workloads.