The tech sector is known for the dominance of software and digital platforms. This focus on computer “bits” enabled companies in the industry to build and distribute their offerings efficiently and cheaply, generating robust margins.

However, the arrival of artificial intelligence (AI) has led to a twist in this story. Tech businesses are now increasingly spending on “atoms,” the label describing capital-intensive physical assets such as data centers, where AI systems are housed.

This industry shift is exemplified in AI tech titan Nvidia‘s recently announced partnership with glassmaker Corning (GLW +1.02%). The deal demonstrates Corning’s ability to see substantial business growth ahead.

Wall Street was sleeping on tech’s swing from bits to atoms, but is now waking up to Corning’s shift from a slow-growth producer of glass products into an AI company. Here’s a deeper look into Corning.

Image source: Getty Images.

Corning’s AI opportunity

Corning has a long history as a materials science specialist in glass used for television screens and fiber optics. Its optical connectivity solutions drove the deal with Nvidia.

Jensen Huang, Nvidia’s CEO, had been saying for some time that traditional copper wiring, such as that used in data center equipment, was approaching performance limits. By partnering with Corning, the semiconductor giant has signaled a transition to light-based data transmission technology.

The partnership grants Nvidia the right to buy up to 15 million Corning shares at an exercise price of $180 per share. In exchange, the two will work together to expand Corning’s U.S.-based optical connectivity manufacturing capacity tenfold.

This manufacturing expansion indicates the magnitude of the anticipated demand to replace copper wiring with fiber optics. After all, the AI infrastructure market is forecast to see massive growth from $75 billion in 2026 to $497.98 billion by 2034, as data centers are upgraded to support artificial intelligence. This provides a substantial multiyear tailwind to Corning’s business.

Today’s Change

(1.02%) $1.95

Current Price

$193.84

Key Data Points

Market Cap

$167B

Day’s Range

$189.50 – $195.00

52wk Range

$48.62 – $211.79

Volume

308.1K

Avg Vol

13.5M

Gross Margin

35.64%

Dividend Yield

0.58%

Is Corning stock a buy?

Nvidia’s adoption of Corning’s solutions is just one significant revenue opportunity for the glassmaker. Nvidia’s new Vera Rubin AI system is massive, weighing about 2 tons and incorporating over 1 million parts. Connecting these components with copper wiring inhibits data transmission at the speeds required by increasingly sophisticated artificial intelligence models. This is why Nvidia turned to Corning’s optical solutions, which enable data transfers at the speed of light.

Moreover, Nvidia’s choice of Corning as a partner is a key endorsement. Nvidia correctly predicted AI’s need for its advanced semiconductor chips, as well as the resulting rise of a new industrial revolution, one where data centers serve as factories producing artificial intelligence.

This latter factor is where Corning is poised to profit as its solutions are adopted by the data center market. In fact, two hyperscale customers entered into large, long-term agreements with Corning comparable to its $6 billion multiyear deal with Meta Platforms.

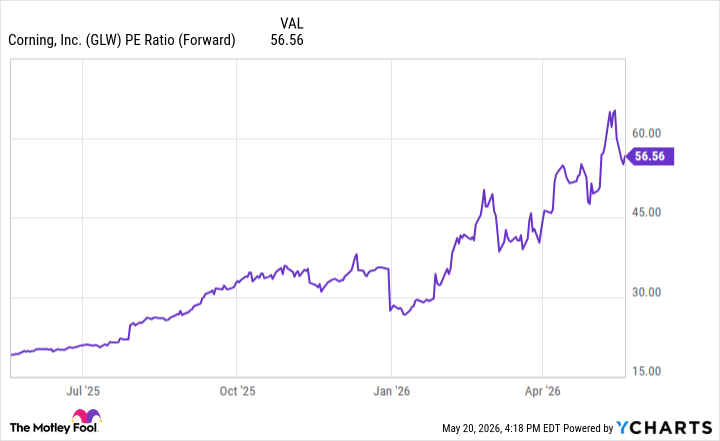

Wall Street began to recognize the bits-to-atoms transition in earnest this year, resulting in Corning’s forward price-to-earnings ratio rising substantially in recent weeks.

GLW PE Ratio (Forward) data by YCharts.

Even so, Corning remains a stock worth investing in for the long term. Because shares hit a 52-week high of $211.79 on May 13, look to buy when the price dips.