The geopolitical conflict in the Middle East has Wall Street excited about oil stocks. Given the supply constraints that the conflict has created, pushing energy prices sharply higher, that makes complete sense. But the truth is that this event isn’t really all that unusual. The energy sector has a long history of being volatile.

That’s why most investors should focus on financially strong integrated energy giants. U.S.-based Chevron (CVX +2.29%) and ExxonMobil (XOM +4.07%) are good choices, as they have both demonstrated their ability to survive the entire energy cycle. However, I’ve chosen to buy the French integrated giant TotalEnergies (TTE +0.94%). Here’s why you may want to buy it, too.

Image source: Getty Images.

Why should you buy integrated energy companies?

The energy sector is inherently volatile. Investors are excited by today’s high oil prices, pushing stocks across the industry higher. However, oil and natural gas are commodities, so they rise and fall over time. Eventually, the geopolitical conflict in the Middle East will end. At that point, the supply constraints that led to higher commodity prices will ease, and commodity prices will likely fall. This might take a while to play out, but history is very clear about what to expect over the long term.

Most investors should tread with caution when buying energy stocks. The industry is actually broken into three parts: the upstream (energy production), the midstream (pipelines), and the downstream (chemicals and refining). The upstream and the midstream are commodity-driven and volatile, often performing differently through the energy cycle. The midstream is fee-based, so it tends to be a more consistent cash flow generator.

If you want to lean into oil prices, you should buy a U.S.-based upstream company like Devon Energy (DVN +4.76%) or Diamondback Energy (FANG +1.65%). But if you are a more conservative investor, stick with integrated giants and their diversified businesses. Having exposure to the entire energy value chain helps to smooth out financial performance over time.

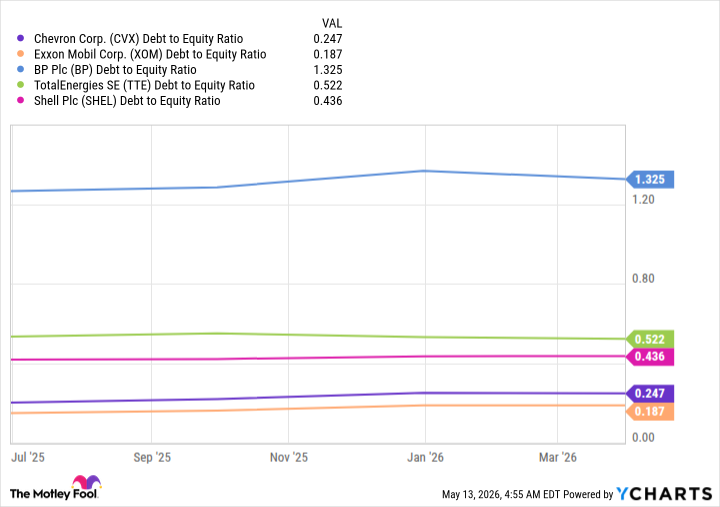

CVX Debt to Equity Ratio data by YCharts

Exxon and Chevron are great examples, noting that both have rewarded investors with decades of annual dividend increases. They also have the strongest balance sheets in their peer group, with debt-to-equity ratios of 0.2x and 0.25x, respectively. (European competitors tend to carry more debt and more cash on their balance sheets.) Chevron’s 3.8% dividend yield gives it an edge over Exxon’s 2.7%.

TotalEnergies stands out for the long term

TotalEnergies is also an integrated energy giant. Its yield is 4.6%, but U.S. investors have to pay French taxes and fees on that, some of which can be claimed back at tax time. So yield alone isn’t the reason why I prefer TotalEnergies. It also has higher leverage, which is the norm for the European competitors. The important difference is clean energy.

Exxon and Chevron have chosen to stick pretty close to their core, only dipping their toes into the clean energy sector. TotalEnergies is making a more concerted effort to expand its clean energy portfolio. In 2025, the company’s integrated power division, which is where its clean energy investments live, accounted for nearly 12% of its business.

Today’s Change

(0.94%) $0.86

Current Price

$92.28

Key Data Points

Market Cap

$205B

Day’s Range

$91.17 – $92.29

52wk Range

$57.13 – $93.67

Volume

963K

Avg Vol

2M

Gross Margin

13.43%

Dividend Yield

4.28%

Essentially, TotalEnergies is using profits from its carbon fuel operations to build a substantial clean energy business. I believe this is a brilliant decision that aligns TotalEnergies with the world’s actual energy demand dynamics. This is the same reason why I own Enbridge (ENB 0.37%), a Canadian midstream company that is also building a clean energy business. I’m happy that TotalEnergies just reported strong earnings, largely thanks to its trading division’s ability to capitalize on volatile energy prices. But I have my eye on the long-term shifts taking place in the energy sector, because eventually oil markets will stabilize and investors will move on to a different high-profile trade.

TotalEnergies is built for today and building for tomorrow

Oil and natural gas will remain important energy sources for decades to come. Investors should have exposure to the sector, with integrated energy giants likely to be the best option for most. Exxon and Chevron are both solid choices for more conservative investors.

However, the shift toward cleaner energy sources is the big long-term trend. Investors shouldn’t ignore it. TotalEnergies allows you to invest in an integrated energy giant while, at the same time, hedging your bets with clean energy. For me, that’s the best long-term solution in the energy patch.