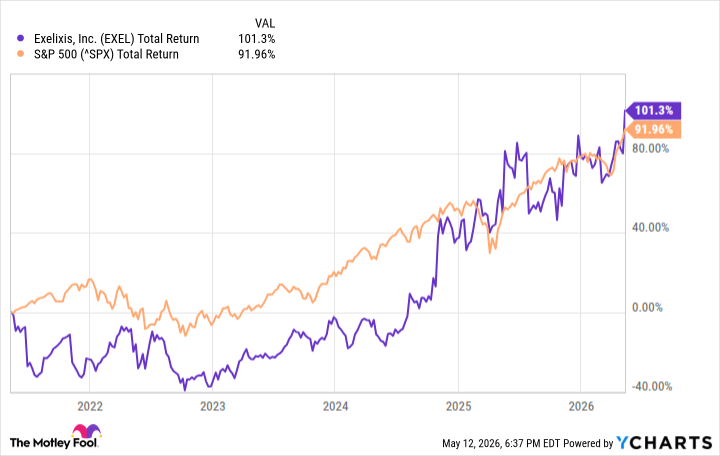

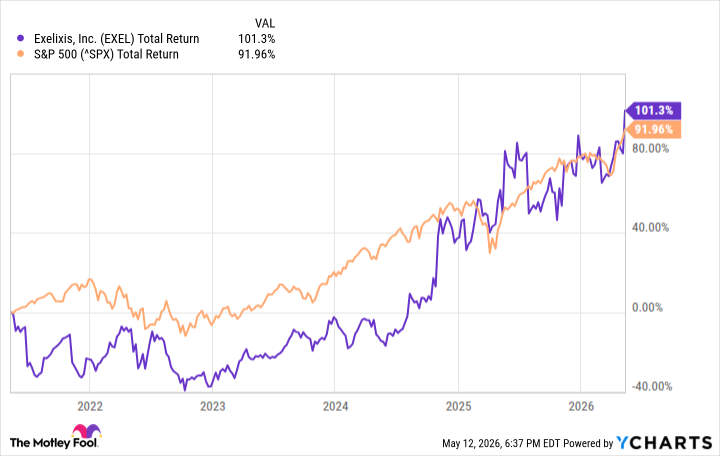

Exelixis (EXEL 1.92%) has been a solid stock to own over the past five years, with its shares climbing 101%, slightly beating out the S&P 500. The good news is that there is plenty of upside left for the biotech company. Over the next five years, the drugmaker could, once again, achieve 2-bagger status (that is, a stock that delivers 100% returns). Here is why.

EXEL Total Return Level data by YCharts

Cabometyx can still drive growth

Exelixis focuses on developing cancer medicines. The company’s most important product is Cabometyx, a drug approved across a range of indications, including some forms of liver and kidney cancer. Now, some might point out that Cabometyx will encounter a patent cliff relatively soon. By early 2030, the medicine should begin to face generic competition. But until then, the therapy can still be a growth driver. In the first quarter, Exelixis’ revenue increased by 10% year over year to $610.8 million. For the fiscal year 2026, Exelixis expects revenue of $2.58 billion at the midpoint, an increase of about 11% from the previous fiscal year.

Image source: The Motley Fool.

One important reason Cabometyx has been a successful growth driver for Exelixis for so long is that not only has it earned several important indications, but it has also established itself as a leader in some niches. For instance, it remains the top-prescribed tyrosine kinase inhibitor — a kind of targeted cancer therapy — in renal cell carcinoma (RCC, the most common type of kidney cancer), and has a strong presence in some other markets as well. Until generics start eating into Cabometyx’s market share, Exelixis will be able to depend on this medicine to drive solid sales growth thanks to its strong market position.

An exciting next-gen cancer drug

If Exelixis’ future just depended on Cabometyx, the biotech company would be in trouble. Thankfully, the drugmaker has been hard at work finding another therapy to succeed its current main growth pillar. The blueprint for Exelixis is to target markets with unmet needs with a drug that can earn multiple indications across several cancer types. The company may have found exactly that with zanzalintinib. This investigational medicine has already completed phase 3 clinical trials (in combination with another drug) in patients with metastatic colorectal cancer. It is currently awaiting regulatory approval for that indication.

This could be an important milestone, considering colorectal cancer is the second-leading cause of cancer death in the world. Clearly, there is a large unmet need here, especially for the metastatic form, which has much lower five-year survival rates than in early stages.

Today’s Change

(-1.92%) $-0.98

Current Price

$50.12

Key Data Points

Market Cap

$13B

Day’s Range

$49.63 – $51.25

52wk Range

$33.76 – $51.63

Volume

71K

Avg Vol

2.8M

Gross Margin

96.44%

But Exelixis won’t stop there. The company is testing zanzalintinib in patients with RCC, with data readouts expected in the second half of the year. Other ongoing clinical trials for the medicine include patients with neuroendocrine tumors, lung cancer (the leading cause of cancer death in the world), recurrent meningioma, and more. Exelixis has high hopes for zanzalintinib. According to some projections, the medicine could hit peak sales of $5 billion.

That’s significant because Exelixis’ current main franchise, Cabometyx, likely won’t reach those heights before it runs into generic competition. The biotech’s sales might decline for several quarters once that happens, but if it can post solid clinical progress for zanzalintinib through the next few years and earn an indication or two for the medicine, the stock could perform well through 2031. There’s even more good news. Exelixis has several early stage pipeline candidates that could also make meaningful progress.

Here’s the bottom line: Exelixis is an innovative biotech company that has carved out a niche in one of the largest and most competitive therapeutic areas in the pharmaceutical industry: Oncology. It currently has a medicine that generates over $1 billion in annual sales and will help it post solid financial results through the end of the decade, and several pipeline candidates, one of which looks particularly promising as a pipeline-in-a-drug. That’s why the biotech’s medium-term outlook seems bright.