, WIRED tested")

Amazon (AMZN +0.55%) has built a dominant position in two growth areas over the years, and these are e-commerce and cloud computing. Shoppers around the world turn to Amazon for a wide range of products, from groceries to mass merchandise and even entertainment like books and movies. And companies have clearly chosen Amazon Web Services (AWS) for a variety of cloud offerings — from storage to artificial intelligence (AI) tools — as it’s become the biggest cloud services provider globally.

All of this has generated massive levels of earnings for Amazon as well as growth quarter after quarter. In the recent period, for example, net sales climbed 17% to more than $181 billion, and profit advanced to $30 billion. And AWS has seen particularly exceptional growth as the AI boom marches on — sales rose 28% for the unit’s fastest growth in 15 quarters.

This is positive, but every bright picture generally also holds a dark spot — something that could weigh on earnings or stock performance, for example. Should you worry about the following trend that’s emerging at Amazon? One metric offers a compellingly clear answer.

Image source: Getty Images.

What’s happening at AWS

Before discussing this trend, it’s key to talk a little bit about what’s happening at AWS — that’s because this trend is clearly linked to the AWS story. As mentioned, this business has experienced tremendous growth in recent quarters due to demand for AI products and services — such as Amazon’s own chips, premium chips from Nvidia, the Amazon Bedrock AI platform, and much more.

Today’s Change

(0.55%) $1.49

Current Price

$272.66

Key Data Points

Market Cap

$2.9T

Day’s Range

$269.95 – $274.00

52wk Range

$196.00 – $278.56

Volume

1.6M

Avg Vol

50M

Gross Margin

50.60%

AWS is a key business for Amazon as it’s traditionally driven profit at the company, and now, as AI demand soars, the door to even higher profitability is wide open. And considering that AWS is the world’s leading cloud provider, it’s well-positioned to capture AI demand.

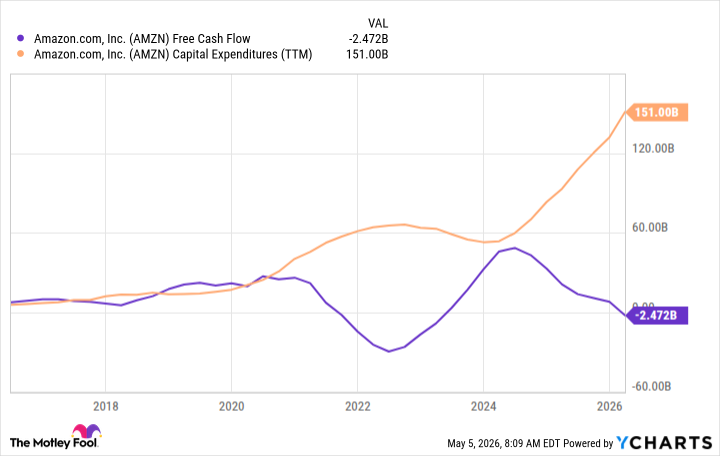

Now, let’s consider the one trend that has worried some investors, and that’s a decline in free cash flow. We can see this has been unfolding as the company increases its capital expenditures to support future growth — Amazon forecasted capex of $200 billion this year.

AMZN Free Cash Flow data by YCharts

Worries about spending

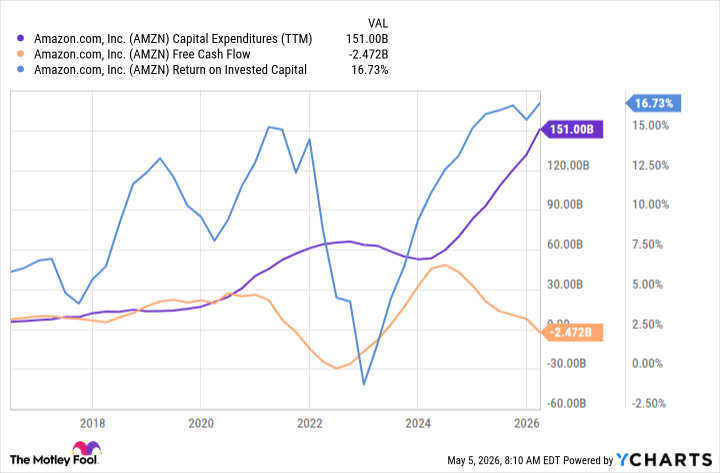

Investors have worried about this spending as they question whether the future revenue opportunity will justify such levels of investment. Here, it’s important to take a look at one particular metric: return on invested capital (ROIC).

We can see that over the past decade, ROIC has declined during periods of increased capex and as free cash flow slips — but it always has gone on to recover and grow, suggesting that Amazon has made wise investment decisions.

AMZN Capital Expenditures (TTM) data by YCharts

So this one metric offers us a compellingly clear message: We shouldn’t worry about Amazon’s declining free cash flow, as history shows us this is part of a known investing cycle — and one that over time has delivered positive results.

Amazon’s investment cycle

Words from Amazon chief executive officer Andy Jassy support this idea. During the recent earnings call, he told investors to expect this pressure on free cash flow, but to also expect growth in ROIC as investments are monetized. Jassy offered a concrete example. When Amazon invests in land, power, chips, and other infrastructure, the company only begins billing customers six to 24 months later — so it takes some time for revenue to start flowing in.

Now here’s more good news: These investments aren’t just useful for a short time, but instead can power growth for years. Jassy says data centers may be useful for more than 30 years, while chips, servers, and other equipment may remain in use for five to six years. So in the early period of monetization, free cash flow suffers, but then the pressure eases as the cycle advances.

“We have been through this cycle with the first big AWS growth wave, and we like the results,” Jassy said. “We expect to feel similarly about this next wave with much larger potential downstream revenue and free cash flow.”

All of this means investors shouldn’t worry about the declining free cash flow trend. Amazon has proven its ability to identify investment areas that will spur growth over time, and we’re in the early stages of one right now. And that makes the stock a fantastic one to hold onto as this AI story continues.