Growth Stocks?")

A supplier issue caused Lucid (LCID 0.56%) to fall short of its first-quarter production and delivery goals. That’s not good and it follows on similar shortfalls in the past, as the company has a habit of overpromising and underdelivering. There’s a reason why the stock is trading near its 52-week and all-time low. Is this an opportunity to buy the stock while it is on the discount bin or should you tread with caution?

Lucid has achieved a lot very quickly

Building a car company is a massive undertaking, but Lucid has done just that. In fact, it increased production by over 100% in 2025. That said, it still only produced 18,378 of its all-electric vehicles in 2025, which is tiny relative to its peers in the highly competitive automotive sector.

Image source: Getty Images.

From a big-picture perspective, Lucid has a lot more work to do before it becomes a sustainably profitable company. And that work will involve making material capital investments in the business. This is why it is selling stock to raise capital, as evidenced by its recent announcement of a $300 million stock sale. That comes along with commitments from Uber (UBER 0.08%) and a private equity firm, which will lead to a total capital raise of just over $1 billion.

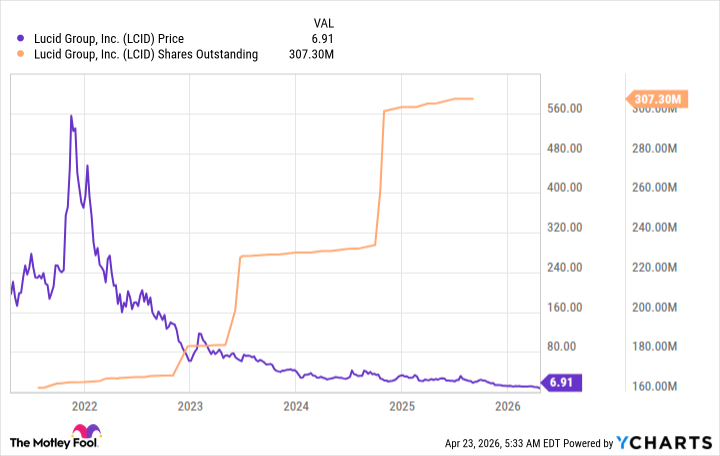

Lucid is selling stock when the stock price is low

All in, it is good that Lucid is still able to raise the capital it needs to continue investing in its business. However, selling stock when the stock price is near an all-time low is not something that most companies want to do. Lucid basically has no choice. The problem for investors is that the company’s ongoing stock sales dilute existing shareholders’ ownership, as they end up owning less and less of the company.

If Lucid succeeds in scaling up its business, it could be a big winner for investors who take the risk of buying the stock today. However, given the company’s still early stage of development, there is a material risk that it will fall short of achieving sustainable profits. If that is the outcome, then even the current low price probably isn’t the bottom for the stock.

Lucid still has a lot of work to do

Only the most aggressive growth investors should consider Lucid today. The stock is cheap for a reason, and the continued production problems and the sale of stock at low prices are both worrying signs. Most investors should probably watch this stock from the sidelines for now.