(2026)")

: Govee, Eufy, Cync")

Last year was a history-maker for America’s leading retirement program, Social Security. Not only did 2025 mark the 90th anniversary of the Social Security Act being signed into law, but it was also the first time in the program’s history that the average monthly retired-worker benefit surpassed $2,000.

For the nearly 71 million people who receive a Social Security benefit monthly (54.1 million of whom are retired workers), there are few announcements more anticipated than the annual cost-of-living adjustment (COLA) reveal from the Social Security Administration (SSA) in October. Since most retirees rely on their Social Security income to cover some portion of their expenses, knowing how much they’ll receive monthly in the upcoming year is of high importance.

Although we’re still well over five months away from this COLA reveal, all signs point to Social Security benefits receiving a “Trump bump” for a second consecutive year — albeit for a different reason. However, this projected boost to benefits doesn’t tell the full story for Social Security recipients.

President Trump preparing to deliver remarks on the energy industry. Image source: Official White House Photo by Molly Riley.

How is Social Security’s annual COLA calculated?

In simple terms, Social Security’s COLA is a near-annual “raise” passed along by the SSA that attempts to mirror and offset the effects of inflation (rising prices).

Imagine for a moment that the cost of a basket of goods and services regularly purchased by seniors increased by 3% from one year to the next. If Social Security benefits remained the same, seniors would see their purchasing power decline (i.e., they wouldn’t be able to buy the same amount of goods and services).

Social Security’s COLA is effectively a raise that’s designed to match the prevailing inflation rate.

For the last 51 years, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) has been the program’s inflation-measuring stick. All of its more than 200 spending categories are uniquely weighted, allowing the CPI-W to be expressed as a single figure at the end of each month.

Even though the CPI-W is reported monthly, only the trailing 12-month (TTM) readings ending in July, August, and September are used to calculate the upcoming year’s COLA. If the average third-quarter (Q3) CPI-W reading is higher in the current year than in Q3 of the previous year, inflation has occurred, and Social Security recipients are due a raise.

The magnitude of the COLA is determined by the year-over-year percentage increase in average Q3 CPI-W, rounded to the nearest tenth of a percent.

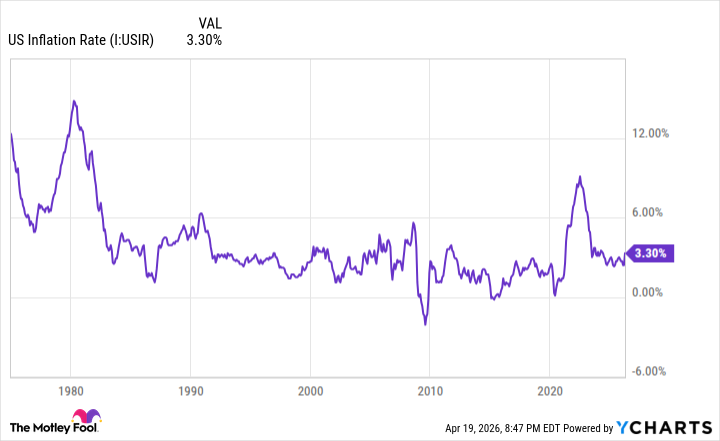

Higher inflation over the last five years has led to a series of above-average Social Security COLAs. US Inflation Rate data by YCharts.

Social Security benefits appear set for a notable boost in 2027, courtesy of Donald Trump

Although U.S. TTM inflation has been above the Federal Reserve’s long-term target of 2% for the last five years, not all aspects of inflation — and therefore Social Security COLAs — have been organic.

In 2026, Social Security benefits increased by 2.8%, marking the fifth consecutive year of at least a 2.5% boost. While some typical factors were responsible for this above-average cost-of-living adjustment, including sticky shelter inflation, President Donald Trump’s tariff and trade policy definitely had a helping hand.

The added duties placed on unfinished imported goods (e.g., steel) often increased final production costs for U.S. businesses, thereby leading to higher inflation. This uptick in prices translated into a beefier Social Security payout for beneficiaries in 2026.

This same dynamic is set up for 2027, courtesy of Donald Trump, but for a different reason.

On Feb. 28, the U.S. and Israel commenced military operations against Iran, leading the latter to shut down the Strait of Hormuz to commercial vessels. Trump’s decision to attack Iran has resulted in the largest energy supply disruption in modern times.

When the supply of an in-demand good or service is constrained, the price of that good or service rises until demand tapers off. Since the Iran war began, crude oil and energy prices have skyrocketed, leading to a tangible impact on U.S. TTM inflation. Even if the Iran war ends soon, the inflationary effects of Trump’s actions will likely be felt for several quarters.

According to nonpartisan senior advocacy group The Senior Citizens League (TSCL), Social Security’s 2027 COLA should match its 2026 raise at 2.8%. Meanwhile, independent Social Security and Medicare policy analyst Mary Johnson nearly doubled her 2027 COLA forecast since the Iran war began: from 1.7% to 3.2%.

Though there’s fluidity to the 2027 COLA forecast with more than five months to go before it’s announced, all signs point to next year’s raise containing a Trump bump.

Image source: Getty Images.

How much of that Trump bump you’ll get to keep is a different story…

On the one hand, a larger nominal-dollar boost to Social Security benefits tends to put a smile on recipients’ faces. However, a larger COLA doesn’t necessarily mean that seniors will benefit.

According to a TSCL analysis released in July 2024, the buying power of a Social Security dollar has declined by 20% since 2010. Put plainly, the CPI-W has done a poor job of accounting for the inflationary pressures that impact seniors.

The problem with the CPI-W is that it’s tasked with tracking the cost pressures faced by “urban wage earners and clerical workers.” These are prominently working-age individuals who aren’t currently receiving a retired-worker benefit. Even though 87% of Social Security recipients were 62 or older as of December 2024, the inflation yardstick used by America’s leading retirement program is focused on the spending habits of working-age Americans.

Compared with those under age 62, retirees spend a higher percentage of their budgets on shelter and medical care services. However, this higher weighting isn’t accounted for by the CPI-W or in the annual COLA calculation.

The other glaring issue is the absence of Social Security’s silver lining.

Retirees enrolled in traditional Medicare often have their Part B premium automatically deducted from their monthly Social Security payout. Part B is the segment of Medicare that covers outpatient services.

Although Social Security beneficiaries enjoyed a 2.8% raise in 2026, Medicare’s Part B premium jumped by $17.90, or 9.7%, to $202.90 per month. This increase is partially or fully offsetting the 2026 Trump bump for most seniors.

A similar fate likely awaits seniors in 2027. The 2025 Medicare Trustees Report estimated that monthly Part B premiums would catapult from $185 in 2025 to $347.50 by 2034, representing a compound annual increase of nearly 7.3%. If the Part B premium continues to handily outpace Social Security’s COLA, not even a Trump bump will matter for retirees.